A unique dynamic has been occurring since the beginning of the year, as short-term rates have been slowly rising while long-term rates have gradually decreased. This dynamic is known as a flattening yield curve, and is generally interpreted as stemming from a decrease in long-run inflation expectations.

In addition to benefiting from subdued inflation expectations, international demand for long-term government bonds has also translated into higher prices and lower yields for those instruments. As a result, rates on the 2-year Treasury note have increased at a faster rate than long-term Treasury bonds with a 30-year maturity. Longer-dated bonds are driven more by inflation expectations than changes in the policy-driven Federal Funds Rate, and recent inflation data suggests that the Fed has kept inflation in check.

Economic growth in the U.S. is stronger than in many other developed economies right now, which has led to a general expectation of rate hikes as the economy strengthens. In other developed economies (such as Western Europe and certain Asian countries), the discussion will likely surround further monetary easing and the need to fight deflation.

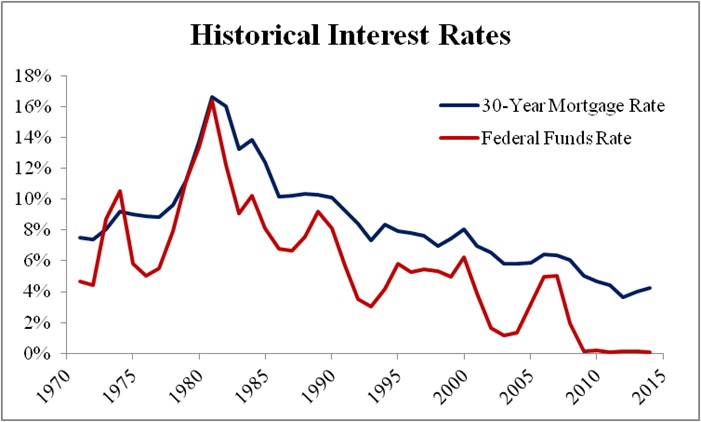

Source: St Louis Fed (FRED)

Of concern for many homeowners and would-be home buyers across the country is how the Fed’s increase in rates would affect mortgage rates. Long-term rates are what affect mortgage rates most, such as conforming 30-year rates. Historically, as the Fed has increase the Fed Funds Rate, mortgage rates tend to lag, remaining tied closer to long-term rates.