In addition to the continued cuts to short-term interest rates, a large driving force behind the stock market’s strong Q4 performance was the expectation (and subsequent completion) of an agreement between President Trump and Chinese President Xi Jinping on a “Phase One” trade deal, which was necessary to avoid a scheduled escalation of tariffs in December. The long-awaited cooling of tensions in the ongoing dispute (which began in 2018, and steadily escalated throughout 2019) was widely viewed as a precursor to a broader agreement in 2020. With an election looming, some have even suggested that a comprehensive trade deal could be in the offing as a potential “October surprise” to boost the president’s reelection chances in November.

And while the “Phase One” deal was certainly a welcome change after months of exhausting posturing by both sides, an examination of the deal indicates that it’s likely more of a placeholder deal than anything substantive, since many of the promises embedded in the agreement are unlikely to be achievable, at least on the proposed timeline.

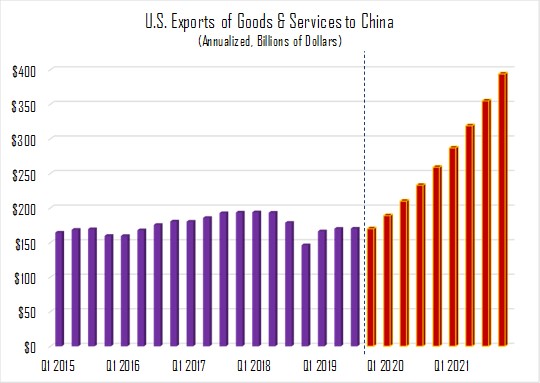

Source: US Census

Among other things, China has pledged in the deal to increase its imports from the United States by $200 billion by the end of 2021 (over its pre-trade war baseline), which would represent a colossal increase from current levels. An expansion of this magnitude would be logistically difficult, particularly because any U.S. gains would come at the expense of Brazil, Australia, and other exporters, and protective moves (perhaps via price wars) would surely follow.