Our most recent quarterly newsletter included a short item discussing the persistent tightness in the labor market, and its ongoing impact on inflation and economic growth. It’s a dynamic that we’ve been tracking for some time now, and it’s an issue that remains as relevant as ever as we head into 2024, with eyes remaining fixated on the Federal Reserve and its interest rate decisions.

So, we thought it made sense to take a bit more time to discuss the current state of the labor market in America, including how we got here, the prospects moving forward, and what it all might mean for the broader economy over the coming months and years.

How did we get here?

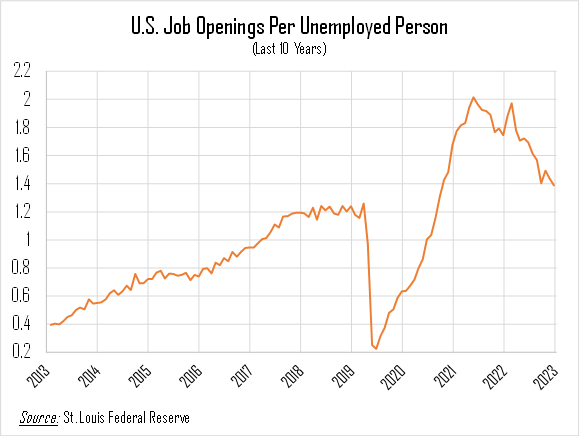

Heading into 2020, the national labor market was in a relatively healthy place. The U.S. economy had added jobs in 112 of the prior 113 months, one of the longest such streaks on record. The unemployment rate stood at a multi-decade low of 3.6%, and annualized wage growth was holding steady at 2.9%, slightly above the prevailing inflation rate of 2.5%. The labor market was also fairly well balanced between employers and employees, with total reported job openings (6.9 million) roughly equal to the number of unemployed people (5.9 million). Workers looking for new jobs could generally find them, and companies searching for new employees were typically able to find a reasonable group of qualified candidates.

But when the COVID pandemic arrived that spring, everything changed; three years later, the repercussions are still being felt. At least four COVID-related dynamics have combined to reshape the labor market in the last few years, for better or worse.

First and most immediately, the demographic makeup of the work force shifted almost overnight. Before the onset of the pandemic, more than 40% of Americans over the age of 55 were still actively participating in the work force (as compared to 83% of the “prime age” working population, between ages 25 and 54). But the shock of the pandemic accelerated the wave of Baby Boomer retirements, causing the participation rate for the older cohort to drop closer to 38%, a level from which it has only very slightly recovered. Most of those COVID retirees won’t be returning to their prior jobs, and it has naturally taken time for younger Americans to age into the work force to take their place. The prime-age participation rate is now back above its pre-COVID levels, but the loss of the older Americans is still notable.

A second dynamic involved industry-specific shifts. The pandemic was most disruptive to sectors like health care, education, and transportation (think: truck drivers), all of which experienced large spikes in work-related stress. Many workers decided that they no longer wanted to work in those industries, and left in search of other roles (many of which allowed for work-from-home opportunities). Since the impacted sectors generally had older work forces to begin with, the combination of changing employee preferences and demographic shifts led to a labor “mismatch”, where too many companies were searching for the same type of employee, and vice versa.

On a related note, the pandemic made changes—at least temporarily—in workers’ geographic desires. Many dense urban settings saw an exodus to more spacious suburban and rural locales, especially as opportunities for remote work expanded. That dynamic may prove to be short-lived (the death of American cities has been overstated many times already in history), but some major cities have struggled to attract workers back in the post-COVID world, especially into the hospitality and tourism industries that had been largely abandoned for years.

Finally, the supply-chain challenges that began in 2020 and persisted throughout 2021 fueled a trend toward “reshoring”, bringing back a number of manufacturing and other jobs that had been outsourced to overseas suppliers over the last couple of decades. That dynamic could prove to be a very positive development for the resilience of the American economy over the long term, but in the short term, it has created yet another source of demand for employees in an already thin labor pool.

Despite all of those headwinds, though, there is plenty of good news in the labor market. As of November’s data, the economy has added jobs for 35 consecutive months, the 5th-longest streak on record, representing a cumulative 14.6 million new jobs. In addition, the total labor force, which had declined by more than 8 million people at the peak of the pandemic, has now recovered to a new all-time high of more than 168 million total workers, nearly 5 million people above its pre-pandemic size.

What we’re looking for in 2024

Still, challenges remain. Despite the gradual recovery in the labor force, demand for employees is still far outstripping supply. In the summer of 2022, there were as many as 2 job openings per unemployed worker, a symptom of an incredibly tight labor market that led to oversized wage gains, adding fuel to the already burning inflation fire. That ratio has steadily declined over the last 18 months, but there are still nearly 9 million unfilled jobs nationwide, as compared to only 6 million unemployed people.

The job opening figure is the lowest in 2.5 years, but the remaining imbalance has kept wage growth elevated, with annualized pay increases still hovering around 4%. For broader inflation to reliably slow down, a properly-balanced labor market is going to be vital. As long as labor market tightness generates wage inflation, prices for goods and services will continue to increase. That dynamic is complicating matters for the Federal Reserve, which enters 2024 with significant uncertainty about how long they will have to wait before cutting interest rates back down to more “normal” levels.

However, the strong demand for labor is also an indicator of a still-robust economy, which makes prognostications of an imminent recession seem less likely. The tight labor market, then, could interestingly help the Fed author the “soft landing” that they’re currently seeking.

Of course, as always, there are other “wild cards” that can come into play. After all, 2023 was the year of A.I., as chatbots and similar technologies promised to reshape the future of the American economy. Could the long-predicted A.I. takeover lead to more workplace automation, shifting the balance back toward employers, and away from employees? Possibly, but those sorts of big-picture shifts are not likely to take place overnight.

In the meantime, most workers have returned to the workplace, even if somewhat reluctantly. The labor market’s recovery will have a significant impact on the economy in 2024, on a number of different levels.