After a frenzied process marked by numerous rewrites and edits, Congress closed out 2017 by passing the most aggressive tax reform bill in decades. Headlined by a significant corporate tax cut, the Tax Cuts and Jobs Act fundamentally rewrote portions of the tax code, promising to impact households and corporations alike.

Sorting out the long-run effects of the tax bill will likely take years, but some winners and losers should be more immediately apparent. We’ll attempt to shed some light on the major impacts of the bill on the economy, the markets, and your household tax return.

Impact on the economy and markets

The main focus of the tax bill is on the corporate side, where the tax rate has been slashed from 35% to 21%. In addition, companies will be allowed to more aggressively expense purchases of capital equipment, and they will also be eligible for a one-time repatriation of “overseas money” at a reduced tax rate. Those changes should significantly increase net corporate earnings, though the gains will vary by sector: telecom, financial, and traditional retail companies are expected to benefit the most, while technology companies (whose stocks have recently been among the strongest performers) will benefit less. From a market perspective, the changes could spark another leg higher for equity markets, as some of the “forgotten” sectors attract renewed attention from investors.

For the broader economy, though, the impact is questionable. Unemployment is already at a several-year low (nearing “full employment” levels), so there isn’t necessarily much room for companies to increase their payrolls. From a cyclical perspective, this is an unusual time to be cutting taxes, since tax cuts (and other fiscal stimulus programs) are typically at their most powerful when there is significant slack in the economy, during or shortly after a recession.

Perhaps not surprisingly, expectations are instead that most companies will use their newfound money (whether from repatriated cash or increased earnings) to make adjustments to their balance sheets. According to a recent BofA/Merrill Lynch survey, the three most likely uses of repatriated cash will be to retire corporate debt, to repurchase stock, or to fund mergers and acquisitions. Only a third of surveyed firms planned to expand capital expenditures, and fewer still are expected to directly increase hiring.

Since the supply of available shares of publicly traded stock is already relatively low after a recent wave of buybacks and mergers, further activity in those areas would continue to be positive for share prices. For investors who maintain an exposure to U.S. stocks, this bill (at least in isolation) should be positive for both earnings per share and stock returns going forward.

Of course, the impact on the federal budget deficit and national debt should also be considered. First, after years of declines, the annual deficit is already beginning to grow again (even before the tax bill), which is unusual for this stage of an economic expansion. For fiscal year 2017, the net budget deficit was estimated at $666 billion, up from $438 billion in 2015. The Congressional Budget Office (CBO) currently estimates that the tax bill will increase the deficit by $200 to $250 billion per year, bringing the deficit as high as $900 billion. By comparison, the highest annual deficit in U.S. history is $1.4 trillion, which occurred in 2009 at the peak of the financial crisis and Great Recession.

There is definitely a case to be made for tax cuts as economic stimulus, but that case draws mostly from previous tax cuts where the overall level of deficits (and accumulated debt) were much lower. Even the rosiest estimates suggest that this bill will add $500 billion to our national debt over the next decade, with average estimates coming closer to $1 trillion, even after accounting for increased economic growth. As a result, Goldman Sachs projects that the current tax plan will push our total accumulated national debt to a level of 85% of GDP by 2021, the highest ratio since the aftermath of World War II. While there is disagreement among economists with respect to the impact of high levels of debt on future economic growth, it is certainly reasonable to question whether this is an appropriate time to be further increasing our national debt.

Impact on your personal tax return

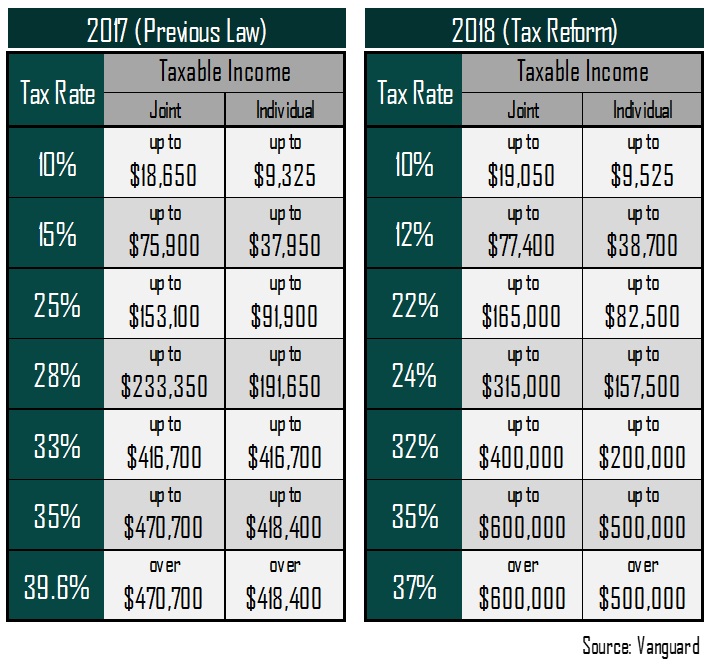

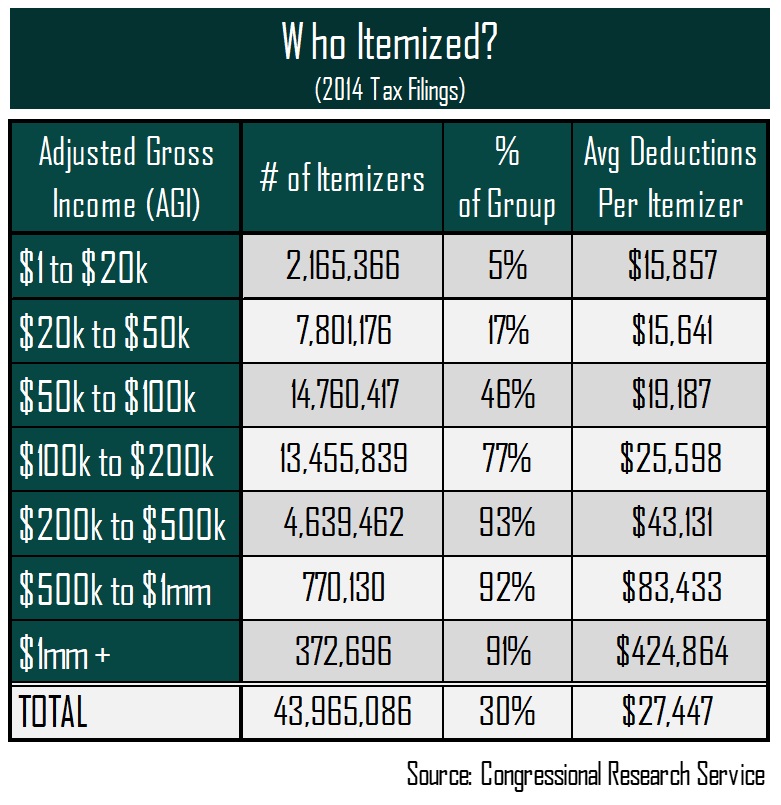

While tax rates will be changing somewhat, the more meaningful changes on the personal side will impact how “taxable income” is calculated, rather than how (much) it is taxed. Before tax reform, about 30% of taxpayers chose to itemize deductions rather than accept the standard deduction. Itemizing allows for deductions for mortgage interest, state and local taxes (“SALT”, including property taxes), charitable contributions, medical expenses, student loan interest, and more. When itemizable deductions add up to more than the standard deduction amount, taxpayers elect to itemize, and the choice to do so can often generate thousands of dollars of tax savings per year.

But many deductions will now be limited: SALT deductions will be capped at $10,000, while mortgage interest for new loans will only be deductible for the first $750,000 of debt (and, notably, home equity loan interest will no longer be deductible at all). Because of those limitations, combined with an increase in the standard deduction—from $12,700 to $24,000 for joint filings—it is now estimated that only 5-10% of taxpayers will itemize. Taxpayers in the upper-middle income range will likely feel this change the most, since 64% of all itemizers had income between $50,000 and $200,000, according to 2014 tax filing records. For some taxpayers, the loss of deductions could end up meaning a significantly higher tax bill in 2018, despite the headline “tax cut” promise. And with fewer taxpayers benefiting from itemization, the incentives to buy homes or donate to charitable organizations could be reduced dramatically in the coming years.

It’s also important to note that another major category of tax-free income—personal exemptions—has now been eliminated entirely. Previously, taxpayers were entitled to an exemption (deduction) of $4,050 for each member of their household, including both taxpayers and dependents. This exemption was in addition to any standard or itemized deductions, combining to create a significant chunk of tax-free income. The elimination of personal exemptions, then, essentially means that the standard deduction isn’t really “doubling”, at all, as many media reports have suggested—in fact, for families with children, the loss of exemptions for dependents could mean that the “effective” standard deduction for the household (deductions plus exemptions) will actually be decreasing. That impact could be offset somewhat by an increase in the child tax credit, but whether the net effect is positive, negative, or neutral will depend largely on a taxpayer’s income level.

A number of other changes were also included in the bill, though most will impact many fewer taxpayers. Of note, the Alternative Minimum Tax (AMT) was retained, but exemption amounts were increased, so that very few taxpayers will owe any AMT. Also, 529 accounts were expanded to allow for funds to be used for private elementary and secondary tuition, not just for college. And while the estate tax was not repealed, the exemption threshold was increased significantly, from $5.49 million to $11 million per individual.

It does bear mentioning that essentially all of the changes on the individual side of the tax code are scheduled to expire after 2025, while most corporate changes are permanent. Finally, any analysis at this point must be considered somewhat premature and incomplete, since it’s too early to tell how state-level tax authorities will respond to the federal changes. Many higher-tax states (like New York) are already seeking to limit the impact of the SALT deduction limit by restructuring the way that their taxes are levied and collected. Some state-level proposals have veered into extremely creative territory, so taxpayers will need to keep their eyes out for state-specific changes that could augment the tax bill’s ultimate impact.

At Cypress, we continue to balance tax impacts with other financial considerations to put our clients in the best possible position to meet their long-term financial needs, while remaining flexible and nimble enough to respond to inevitable changes in the financial and economic landscape. If past is indeed prologue, then this tax reform bill will likely be subject to many revisions over the coming decade, particularly if control of Congress and/or the White House changes hands. If you have any questions about how this bill might affect you or your business, feel free to give us a call.

Information found in this blog post is not intended to be individualized tax advice or legal advice. Please discuss such issues with a qualified tax advisor.