From an economic perspective, the impact of Presidential election outcomes tends to be greatly overstated. Chief executives do not actually exercise much direct control over economic policies, and even when they do, the stock market’s reactions are unpredictable. There is little compelling evidence that the economy (or the market) does better when either a Republican or a Democrat is in office, and the evidence becomes even muddier when we add “control of Congress” into the equation. For the most part, it’s typically a good idea to keep politics far away from investing.

That said, this election year may turn out to be a bit different, if only because tax policy is on the ballot. That’s because the 2017 Tax Cuts and Jobs Act (TCJA) put in place dozens of tax cuts and other tax-related provisions, the vast majority of which are scheduled to “sunset” at the end of 2025. Vast portions of the tax code, then, will have to be renegotiated (if not rewritten entirely) at some point next year, and the control of both Congress and the White House will have a significant impact on the direction that those discussions end up taking. Already, both Presidential candidates have put forth proposals for what they’d like to see happen with tax policy, and there are significant differences. We’ll take a look at where the candidates agree, where they do not, and the potential implications of the different policy proposals.

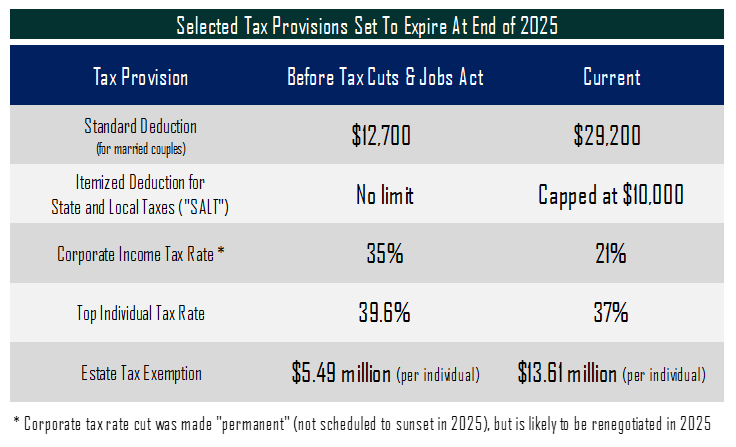

What’s expiring

The TCJA was a wide-ranging tax law, impacting nearly every area of the tax code, and dozens of its provisions (especially those targeting individuals, as opposed to corporations) are scheduled to expire in 2025. Some of the most significant, though, involve deductions, both standard and itemized. When calculating taxable income, each individual has the option to either take the standard deduction (a set amount that any taxpayer can claim) or to instead “itemize” deductions, which can and do vary from one household to another. The major categories of itemizable deductions include mortgage interest, charitable donations, and deductions for state and local taxes paid (generally state income tax and local property tax).

The TCJA made two drastic changes to the math surrounding these deductions. First, the standard deduction was nearly doubled, from a level of $6,500 per individual to $12,000 (this figure is adjusted each year for inflation, and now stands at $14,600). In addition, the deduction for state and local taxes (commonly known as the “SALT” deduction) was capped at $10,000 per household. Since the SALT deduction is one of the largest itemizable deductions for most households, this change substantially impacted the proportion of taxpayers who elected to itemize.

Before the TCJA was enacted, roughly 30% of taxpayers chose to itemize, representing nearly 50 million tax returns. By 2020, the IRS reported that only 10% of tax filers had elected to itemize, essentially all due to the TCJA changes. For many middle-income taxpayers (especially those in high-tax states), this shift meant a stealth tax hike, as the loss of a once-valuable deduction increased taxable income. Many states subsequently tried to find workarounds to the SALT cap, with limited success.

In addition to the altered deduction math, the TCJA also cut marginal tax rates for individual filers (including slashing the top tax bracket from 39.6% to 37%), doubled the child tax credit, introduced a 20% deduction for pass-through business income, and doubled the estate tax exemption (which now stands at a combined $27.2 million for married couples). For some taxpayers, these changes have had significant impacts on their tax burden. Interestingly, while the corporate tax rate has been a common topic on the campaign trail, it is not technically up for debate in 2025, since the TCJA made the corporate tax cut (from 35% to 21%) permanent. However, given the current climate, it seems likely that any tax-related negotiations will eventually evolve to include the corporate rate.

What’s being proposed

Campaign season tends to bring out a laundry list of “wants” and desires, some of which are meant to spark discussion but unlikely to actually generate legislation in the immediate future. One such example is the Harris campaign’s widely-publicized proposal to begin taxing unrealized capital gains for individuals with wealth greater than $100 million. A tax that would be more of a wealth tax than an income tax, some proponents have likened it to a property tax, albeit on a much broader scale. While the inclination to tax the super-rich has broad populist appeal, the proposal is fraught with logistical complications, and implementation would likely be messy. Depending, of course, on the ultimate control of Congress, this proposal seems more likely than not to be sidelined in favor of more immediate concerns.

As mentioned above, the corporate tax rate is not technically up for debate in 2025, but both candidates have taken a position, and they are predictably very different. VP Harris has proposed increasing it back to 28%, whereas former President Trump has promised to cut it even further, to 15% (albeit only for companies who produce the majority of their goods/services inside the U.S. borders).

One area of potential agreement surrounds the SALT cap, as described above. In mid-September, the Trump campaign officially announced its support for scrapping the SALT cap, a provision that he of course first signed into law. While VP Harris has yet to make an official declaration, she has previously signaled support for such a provision, especially since some of the most heavily impacted taxpayers reside in reliably “blue” states including California, Illinois, New York, and New Jersey. Other miscellaneous provisions—like exempting tips from taxable income, or providing increased tax deductions for start-up small businesses—may still prove important, but could also fall into the “meant to spark discussion” category.

Other considerations

One thing that seems clear, bearing a major change of heart: under either candidate’s plan (as currently proposed), deficits and debt will expand. According to the Penn Wharton Budget Model, the Harris proposals would add $1.4 trillion in debt over the next decade, while the Trump proposals would add $3.0 trillion. That may be good for economic growth, but of course comes with other concerns about long-term sustainability. In addition, other issues—like trade policy and immigration policy—could have an even larger impact on the broader economy. For individual households, though, the tax policies will bear close watching, and control of Congress may be the most important determinant of future direction. If you have questions about the potential impacts on your own personal tax situation, we are always here to help.