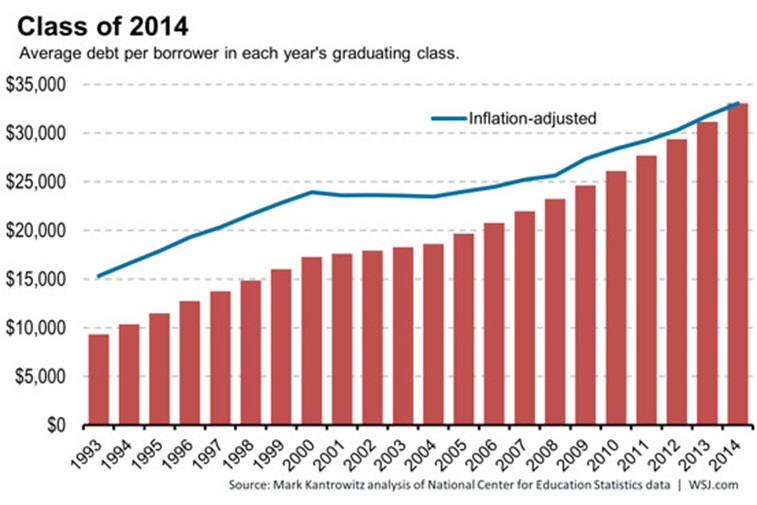

As college tuition costs have marched ever higher over the last decade, student loan balances have risen along with them, to the point that they now represent a meaningful portion of many household balance sheets. The numbers are staggering: one in five households carry some student debt, a rate that has more than doubled since 1990. Total outstanding student debt is now in excess of $1.2 trillion, which far exceeds the aggregate level of consumer credit card debt (currently around $800 billion). The average student loan balance is roughly $28,000 per borrower, and a full 13% of indebted households hold a balance above $50,000. For the most recent graduates, the Wall Street Journal reports that average loan balances at graduation exceed $33,000, up from $20,000 a decade ago.

These loans are clearly concentrated among the younger generation, but they do impact older generations as well (either stemming from their own advanced degrees or from borrowings on behalf of their offspring). And while salaries for recent college graduates are typically high enough to service those debt balances without too much of a problem, it’s clear that the loans are having a wide impact on the financial decisions of the younger cohort. Studies have shown that millennials are delaying marriage, shunning homeownership, and having children at increasingly advanced ages. Stresses from student loan debt are contributing to–if not entirely responsible for–all of those dynamics.

The inability to build wealth in the early working years could have long-lasting impacts on millennials’ ability to meet their lifetime financial goals. Given that fact, it’s surprising that comparably little has been said or written about strategies for getting out of (or avoiding) that debt. Whether you’re trying to figure out how to put your kids through college or already struggling with debt of your own, this discussion should put some context around a burgeoning financial struggle.

Look to your home

One of the biggest mistakes that many households make is a failure to think about their various debt balances in their totality. As a result, they’ll often unwittingly make outsized debt payments to their lowest-rate loans while allowing a high-rate loan to continue piling up punishing interest charges. There are often opportunities to concentrate (or consolidate) debt into the most favorable vehicles, and mortgages on primary residences are the most beneficial of all debt instruments.

If you own a home and also carry a student loan debt balance, it may be advisable to increase the amount of your mortgage (tapping your home equity) in order to pay down the higher-rate loan debt. Such a move could have two benefits–a decrease in the rate (because mortgages are secured by the house, while student loans are unsecured), and an increase in the tax-deductibility of interest payments (since there are fewer limitations on deductions for mortgage interest than for student loan interest).

While you generally won’t be able to increase your mortgage above 80% of the house’s value via a home equity loan, it’s worth checking to see what your options may be, as your budget and life circumstances allow. Home equity can often be a very valuable debt-management tool.

Look to your family

According to Rohit Chopra, the student loan ombudsman for the Consumer Financial Protection Bureau, the seeds of the increase in student loan debt lie in the financial crisis of 2008-09, though not in the way we might first think. At a conference earlier this year, Chopra related that “what we found is that because American families lost so much in home equity [and] wealth, what they would typically have contributed to their child’s education really shrunk. And so it shifted a lot of costs from one generation to another, leading to a huge jump in debt.”

In essence, parents who wanted to pay for their children’s education were unable to do so because cash flow and investment balances were tight. Now, with the stock market having recovered to record highs (and unemployment at several-year lows), it’s likely that the stresses on the older generation have eased somewhat, and they may be in a better position to help now than they were during the actual years of education. For parents who still have the desire to help their children, there are options available.

First, the parents can elect to help via an outright gift to their heirs (gifts that stay within annual exclusion limits are best, so as to avoid giving taxable gifts), in order to help pay down the loan balance. Alternatively, an intrafamily loan can be arranged, with the parent essentially taking the place of the original student loan lender. Intrafamily loans can often serve a dual purpose for families–the student/borrower is able to lower his rate to a more manageable amount, and the parent/lender is able to earn a reasonable rate of interest from a known and (presumably) creditworthy counterparty.

Rates on current student loan balances can be as low as 4% or as high as 8% or above. For parents who are currently invested in fixed income instruments that pay only 2% or 3% (which is common in the current environment), they could be doing as well or better for themselves by lending to their children instead, saving the kids interest in the process. If the parents are so inclined, they could even forgive a portion of the loan each year by taking advantage of the annual gift tax exclusion (currently $14,000). Given the various benefits, it’s perhaps unsurprising that intrafamily loans have increased in popularity in recent years, even becoming a standard part of some families’ estate planning efforts.

Take preemptive strikes

Of course, the best way to manage student loan debt is to minimize or eliminate it on the front end. For parents (and students) who have not yet begun paying tuition or accumulating loan balances, it’s never a bad time to start having conversations about optimal education financing strategies.

Intelligent usage of Roth IRAs and Section 529 plans can help invest saved funds in a tax-optimal manner, which can help reduce the overall financial burden. Also, direct tuition payments made by family members are exempt from gift tax consequences when paid to cover a current student–that is, if a grandparent or other family member wants to pay for a child’s education, he or she can do so without giving rise to a taxable gift, as long as payments are made directly to the institution (and not to the student). For individuals or families who are looking for ways to minimize the size of their taxable estate, this unlimited exemption can help to meet multiple goals simultaneously. Proper education planning is an integral part of both retirement planning and estate planning–doing the right things in one area can dramatically help your progress in the others.

The views expressed are not intended as a forecast, a guarantee of future results, an investment recommendation, or an offer to buy or sell any securities. The information provided is general and should not be construed as investment advice or to provide any investment, tax, financial or legal advice or service to any person.