Maintaining a happy marriage is always a bit of a balancing act: two individuals come into a relationship from distinct backgrounds, each having developed his or her own attitudes toward work, family, money, and how to prioritize their goals. Perhaps not surprisingly, financial matters are among the most contentious issues between married couples, sparking more than a third of all marital disputes. According to expert research, financial disagreements and stresses are among the leading reasons given for divorce, alongside infidelity and physical abuse.

As the financial pressures continue to mount on many American families, these stressful conversations are becoming more frequent and more difficult to navigate. We’ll consider some of the most common financial conflicts among married couples, while also providing strategies for managing (and hopefully working through) those disputes.

What are the most common disagreements?

Spender vs. Saver

It’s often said that “opposites attract”, and financial matters can be included in that aphorism. In almost every married couple, one spouse is more inclined toward saving and accumulating financial assets, while the other focuses more on current consumption, spending money more freely in the here and now. Of course, not all couples are polar opposites in this regard, but even in marriages where the spouses are fairly similar in their feelings toward spending and saving, the minor differences can seem to become magnified over time, and resentment can fester.

Separate vs. Combined

The decision whether to combine finances or keep them separate is often one of the first financial decisions a married couple has to make, but it’s also commonly one of the most difficult and contentious. There are strong arguments to be made for either decision, and both emotional and practical issues must be considered. Holding assets jointly can be more efficient from a daily management perspective (and can help streamline the estate planning process), but emotional issues can be very powerful, especially for previously-divorced individuals.

Risk Tolerance

Attitudes toward risk inform almost every financial decision a married couple has to make, and not just inside of an investment portfolio. Deciding how much cash to hold in an emergency fund, whether to buy or rent a home, how much house to purchase (and/or how much of a down payment to make), and even deciding what age to consider retiring are all decisions that will be informed by each spouse’s tolerance for risk. It’s rare for spouses to be completely aligned from a risk perspective, and again, the differences tend to become magnified over time.

Supporting Family Members

Of course, financial matters have a way of extending beyond just the spouses to include other family members. Deciding how much to contribute to a child’s college tuition (or whether to support them financially as adults), how to care for aging parents, or even providing assistance to a sibling in need can all turn into stressful decisions. Even spouses who are in lockstep managing a household budget can differ wildly when the financial conversations move outside the house to include extended family.

Debt

Debt is an increasingly common issue for young married couples, particularly millennials who are graduating with record levels of student loan debt. Indeed, a reluctance to bring debt into a marriage is one of the leading reasons given for an increasing average marriage age (and declining marriage rates).

Strategies for resolving financial conflicts

Communicate Often

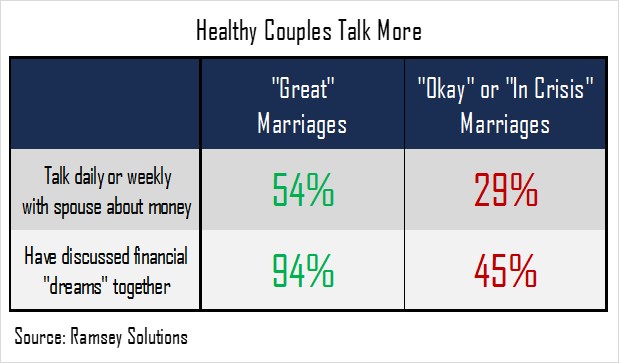

Correlation may not imply causation, but research shows that individuals in healthy marriages have more frequent (and more in-depth) conversations about money, by a 2-to-1 margin. Financial conversations are often fraught with emotion, and a wide variety of insecurities come into play. It’s vital to remain open and honest at all times, and to keep lines of communication open. If you feel the need to start hiding purchases from your spouse, that’s probably an indication that you’re not on the same page, and that some more in-depth discussions about money matters are required, sooner rather than later.

Delegate Responsibilities

One way to bridge the gap when financial conflicts arise is to share responsibilities according to each spouse’s tendencies and strengths. If one spouse is a saver and the other is a spender, maybe the saver can be put in charge of retirement savings (and investments), while the spender can be the one to plan out and coordinate some of the major lifestyle expenses, like car purchases, vacations, and more.

Focus on Lifestyle Goals, Not the Money Itself

It may seem counterintuitive, but many arguments about money aren’t actually about money after all, but about broader lifestyle goals, and how to expend our naturally limited resources (whether time, money, energy, or a combination of the three). We all have differing priorities, and money is merely a means to our many ends in life. Shifting the conversation to the “why” instead of the “what” can often clarify things and reveal room for agreement and compromise. If we stop talking about money for money’s sake, and talk instead about what that money can do for us—and what we want or need it to do for us—then we can take some of the emotion out of financial conflicts.

Ultimately, most married couples agree on what they want out of life (and out of their relationship together), but simply disagree on how they want to obtain it, and on what timeline. Financial conflicts, then, often deal more with questions of when and how to achieve those goals; recognizing that there is more common ground than difference can often be the first step toward solving seemingly intractable disputes.

Of course, some conflicts are more difficult to resolve than others, and in these cases, compromising is key. We can combine finances in some areas, then, but not in all; we can take large risks with one “pot” of money, but maybe not the entire retirement nest egg. When we stop thinking about money in binary spending/saving terms, and instead view our financial disputes on a spectrum, the disagreements can begin to seem relatively minor, and manageable.

Regardless, understanding your current financial situation—including its strengths, weaknesses, and opportunities for improvement—is a vital starting point. Financial arguments often stem from insecurity and fear, and a lack of knowledge can fuel that worry. Working together to establish and maintain a long-term financial plan can minimize that insecurity, enabling both spouses to have a healthier relationship with money and with each other. Money and emotion can never be separated, but they can be reconciled.