In an article written earlier this year, we noted a recently-settled class-action lawsuit brought by the employees of Lockheed Martin against the company, alleging breaches of fiduciary duty within the firm’s 401(k) plan. That settlement was followed by a similar one this August, this one involving 190,000 employees and retirees of Boeing, the world’s second-largest defense contractor. While the details of the cases vary slightly, both involve the use of investment advisors and funds that did not align with the best interests of plan participants, including poorly-chosen or overly expensive investment options.

The logical question for retirees everywhere is, if these issues exist at some of the largest 401(k) plans in the country (Boeing boasts roughly $48 billion in plan assets, Lockheed about $27 billion), do the participants of smaller plans have any chance of getting a fair shake? After all, across the 401(k) landscape, nearly 60% of active plans have total assets of less than $2.5 million, a far cry from the tens of billions at Boeing and Lockheed. Accordingly, the average plan can be expected to have much lower bargaining power with financial firms than the Fortune 100 companies, and theoretically much more vulnerability to breaches of duty.

Not surprisingly, the Department of Labor (DOL) has taken notice, recently issuing a proposed new fiduciary rule, which could redefine the types of investment advice that would qualify an advisor (or custodian) as owing a fiduciary duty to participants. So, just what is a fiduciary? And how does it affect you as a 401(k) plan participant, or as an investor more generally? We’ve put together a quick primer, so that you can understand just who qualifies as a fiduciary, and why it matters to you.

What is the fiduciary standard?

In the investment industry, the fiduciary standard is the highest standard of care that an advisor can owe a client, whether that client is a 401(k) plan participant, an individual client, or otherwise. Generally speaking, there are two standards to which advisers can be held, roughly corresponding to two different compensation structures.

The suitability standard applies to investment brokers, who typically work for large investment companies (broker-dealers) and earn their compensation based on commissions from the sale of investment products. Essentially, the suitability standard requires only that the broker recommend securities that are consistent with the investing objectives and time horizon of the client. The suitability standard does not require that the broker put the clients’ interests ahead of his or her own, and conflicts of interest often follow.

A broker may, for example, be incentivized to steer a client toward a higher-fee product instead of a lower-fee product with similar investment characteristics, simply because the broker stands to earn a higher commission from the sale of the higher-fee product. While the broker may still choose to recommend the lower-fee product, he is under no legal obligation to do so.

The fiduciary standard, meanwhile, typically applies to Registered Investment Advisors (RIAs), as registered with either the SEC or the state securities regulators (a distinction that depends on the size of the firm). These advisors are normally compensated via fees paid directly by the client—they are thus often referred to as “fee-only” advisors, and they generally do not earn money from product sales commissions. As mentioned earlier, the fiduciary standard also frequently applies to 401(k) plan administrators, who may or may not otherwise be in the business of giving investment advice.

Unlike brokers subject to the suitability standard, an advisor operating under the fiduciary standard must place the clients’ interests above his or her own. Any sources of compensation and potential conflicts of interest must be disclosed (often in writing), and breaches of this fiduciary duty can carry stiff penalties, including loss of professional licenses. In the investment world, the fiduciary standard is the most protective for clients, and it creates a special relationship that is rare in the business world.

That said, there is room for both approaches within the financial industry. For a given client, there are various situations where one type of advisor may be preferable over the other. The problem comes when a client thinks he or she is talking to an advisor who owes a fiduciary duty, when in fact there is none. In that circumstance, misunderstandings and suboptimal outcomes are likely to occur.

But, it’s complicated…

While the distinction between the two standards might seem fairly straightforward, such simplicity is of course rarely the case—if it were, then the DOL wouldn’t feel the need to issue new rules clarifying the fiduciary standard.

Most confusingly, it is possible for the same advisor to be subject to both the suitability standard and the fiduciary standard, even while working with the same client. This is most often the case with “dually registered” advisors, who operate as both RIAs and investment brokers. In this case, advisors will often serve in a fiduciary role when giving general advice or engaging in financial planning, but shift over to the suitability standard when it comes time to recommend investments. This “two hats” approach might seem crazy, but it’s fairly common, and it breeds significant confusion. Remember: just because someone refers to himself as an “advisor” doesn’t necessarily mean that he’ll operate as a fiduciary.

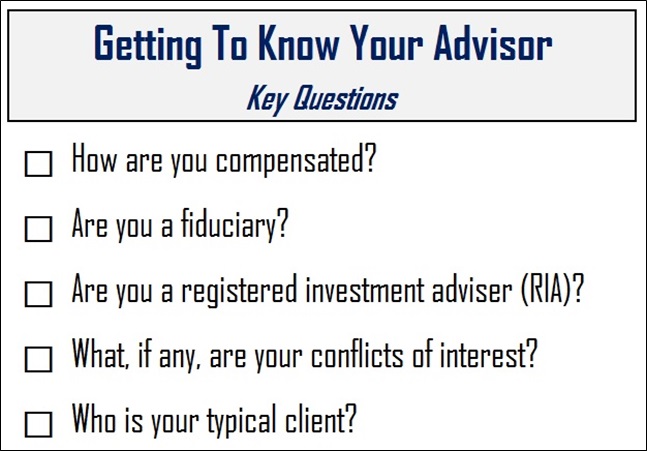

Is my financial advisor a fiduciary?

It’s hard to know unless you ask. The only way to know for sure is to thoroughly interview your advisor before engaging his or her services, and to have an open dialogue with them. First and foremost, it’s important to understand how your advisor is being compensated. If your prospective advisor earns commissions from product sales, ask how that might affect the advice they give. If their answer seems unsatisfactory, then you may want to consider interviewing another advisor.

At Cypress, we take great pride in serving as a fiduciary to all of our individual clients, including providing advice on their workplace 401(k) options. We also offer fiduciary services to 401(k) plans and their participants, in order to help prevent lawsuits like those at Lockheed and Boeing. If you need help navigating your personal or 401(k) investment options, either as a participant or administrator, we can help.