Tax-deferred retirement accounts are an integral part of any well-designed financial plan, but they do come with certain drawbacks. Some individuals who have been particularly aggressive deferring income into 401(k) plans or IRAs might eventually find that a significant portion of their net worth—if not essentially all of it—is tied up in one type of retirement account or another. If a major expense then comes up unexpectedly, having too much cash invested in a retirement plan can be a significant limitation.

That’s because with a few exceptions, any “early” withdrawal from an IRA (a distribution taking place before the account holder has reached age 59 ½) is subject not only to ordinary income taxes, but also to a 10% penalty on the amount withdrawn. However, the Taxpayer Relief Act of 1997 (the same act that created the Roth IRA, among other tax credits and relief programs) established a number of exceptions to that 10% penalty for withdrawals from an IRA. What, then, are the exceptions, and when can they be used to your advantage? We’ll discuss the four main categories of exceptions established by the 1997 Act, and how (or if) you can use them to help cover your own expenses.

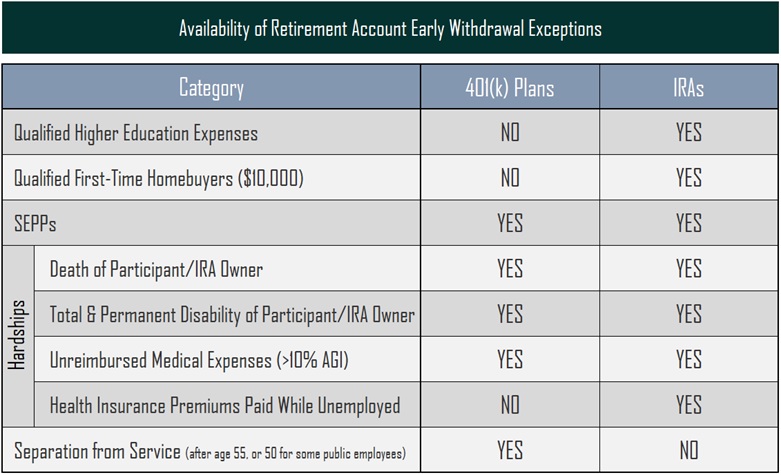

Qualified education expenses

The first exception category is reserved for qualifying higher education expenses, as defined by IRS code. An account holder can, without penalty, withdraw funds at any age if those funds are used to cover tuition and related expenses at an IRS-approved institution (generally speaking, any post-secondary school that meets federal student aid requirements, either public or private). The withdrawal (and payment) must be for an academic period beginning in the same tax year as the withdrawal, or in the first three months of the next tax year. Finally, the education expense exception can be used for the account holder’s own education, or that of his/her spouse, children, or grandchildren. Note that the education exception is not available for funds invested in a 401(k) plan, only an IRA.

There are certain questions as to which types of expenses can qualify for the exception, but tuition and required fees, books, supplies, and other required equipment are generally considered to qualify. Room and board expenses are a somewhat murkier area, but IRS guidance suggests that room and board will qualify as long as the student is enrolled at least half-time in an approved degree-granting program.

Qualified first-time homebuyers

The second category is reserved for first-time homebuyers, and it is limited to a lifetime exception of $10,000, to be used toward a down payment on the purchase of a primary residence. Again, this exception is not available for funds invested in a 401(k) plan, only an IRA. While IRS guidance is somewhat limited, the wording of the exception does indicate that if a married couple purchases a home together, each spouse can use their own $10,000 exception, for a total of $20,000.

Notably, despite the name, this exception does not specifically require that the residence in question be the first home that the individual has ever purchased—in order to qualify, the IRA holder need only have not owned a principal residence at any time during the previous two years. Therefore, it’s at least theoretically possible for someone who has previously owned a home to still qualify for the first-time homebuyer exception. Either way, the exception can only be used once per taxpayer in their lifetime.

SEPPs

A third category is most useful for individuals considering early retirement, utilizing an approach called “Substantially Equal Periodic Payments” (SEPPs). SEPPs allow account holders to begin accessing retirement funds immediately at any age, provided that the payments are made as part of a series of ongoing annual payments (essentially, an annuitization of the retirement account). The rules surrounding SEPPs—and how to calculate appropriate annual amounts—are complex and beyond the purview of this discussion.

However, regardless of the withdrawal method and amount, once a system of SEPPs is established, the account holder will need to continue making annual distributions for at least five years or until he or she reaches age 59 ½, whichever is longer. During this period, distributions larger than the established SEPP are not allowed, and if a larger distribution is made, prior SEPP distributions become retroactively subject to penalties. Therefore, SEPPs are most useful for early retirees who need a stable stream of income, rather than for active workers or individuals looking to cover a large one-time expense. Unlike the two previous categories, SEPPs are available in 401(k) plans, provided that the account holder is no longer employed by the 401(k) plan sponsor.

Hardship withdrawals

The final category is one that most individuals hope they will not have to use, since these exceptions all essentially require that something bad first occur. There are four main “hardship withdrawals” that can qualify for a penalty exception, including the death of the account holder, the permanent disability of the account holder, amounts withdrawn to cover medical expenses in excess of 10% of Adjusted Gross Income (AGI), or health insurance paid during a period of unemployment. Note that simply losing a job (or having major medical expenses) might not necessarily qualify an individual for a hardship withdrawal; certain thresholds (or other prerequisites) also need to be met.

Source: IRS

Other considerations

Just because an exception is available doesn’t mean that it should be used. After all, even absent a penalty, ordinary income tax will still be owed on any Traditional IRA withdrawal. It’s also important to note that IRAs and 401(k) plans have different benefits and drawbacks: among other things, IRAs cannot offer loans, but 401(k) plans can, although 401(k) plans have fewer available penalty exceptions.

Also, while these IRA exceptions apply to both Traditional and Roth IRAs, Roth IRAs are unique in that taxes and penalties can only ever apply to investment earnings accrued within the account—the initial contribution amount to a Roth IRA can always be withdrawn without tax or penalty, making the Roth a very powerful and nimble tool for retirement savers with uncertain or lumpy expenses.

Regardless, any withdrawal from a retirement account must be carefully considered, since tax-deferral benefits, once lost, are often lost forever. At Cypress, we are always looking for ways to maximize the benefits of tax-deferred retirement accounts for our clients, while also preserving flexibility and liquidity.

The information provided is for educational purposes only and is not intended to provide any investment, tax, or legal advice.