As the Federal Reserve Board continues to consider whether (or when) to resume increasing the target for its benchmark Fed Funds Rate—which has now stood below 1% for a record 96 straight months—investors everywhere are taking a second look at their fixed income holdings, lest they find themselves improperly positioned for an eventual end to what is now a 35-year bull market in bonds.

It has become taken almost for granted that interest rates must some day rise, but that statement (or belief) alone is insufficient to prescribe action. What happens with one group of interest rates may or may not also happen with a different group—in other words, it’s not just “if” you own bonds that matters, it’s what types of bonds you own that will determine your portfolio’s performance.

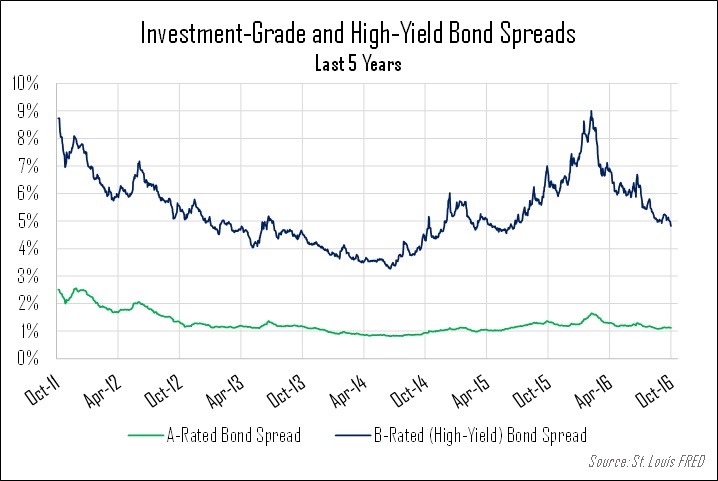

A closer look at the behavior of bond yield spreads can better illustrate both the difference between various types of bonds and the likely market response to any “rise in rates”. Helpfully, BofA/Merrill Lynch regularly tracks several different bond yields, from Treasury notes to A-rated corporate bonds to high-yield “junk” bonds and beyond. Calculating the yield spreads—the gap between the yields on the bonds in question and prevailing “risk-free” Treasury rates—can isolate the performance of a specific group of bonds from the broader fixed income environment.

As any high-yield bond investor is likely already aware, spreads for high-yield bonds spiked dramatically in 2015, as a plunge in the price of oil sparked widespread concerns about the liquidity and solvency of a wide variety of energy companies (who have been among the heaviest issuers of high-yield debt in recent years). Their higher-rated corporate bond cousins also saw a small increase in their yield spreads, but nowhere near as extreme an increase as was seen in the high-yield space. This year, as oil prices have stabilized, high-yield bond spreads have consistently declined as well, now nearing levels that were last seen before the oil price crash.

It’s telling to note that while high-yield bond spreads have continued to compress in recent weeks, spreads for higher-rated corporate bonds have been stable, if not widening slightly. That divergence can be credited almost entirely to expectations of future Fed rate hikes. If and when the Fed does resume raising rates, it’s likely that the highest-quality bonds will be the ones most heavily impacted in the near term. One of the central goals of the Fed’s zero-interest-rate policy was, after all, to force investors into riskier assets, and high-quality corporate bonds quickly became something of a portfolio surrogate for Treasury bonds, which suddenly had yields too low to be worth owning in many portfolios.

As rates on Treasury bonds gradually return to more normal levels, it stands to reason that their surrogates would be the first things sold as investors move back into Treasuries and other “risk-free” instruments. High-yield bonds can be expected to feel the pinch as well, but their higher yields should insulate them somewhat, while industry-specific factors continue to play a role. Maintaining exposure to a variety of fixed income instruments remains the prudent move.

The views expressed in this post are not intended as a forecast, a guarantee of future results, an investment recommendation, or an offer to buy or sell any securities. The information provided is informational and should not be construed as investment advice or to provide any investment, tax, financial or legal advice or service to any person.