In the aftermath of the Brexit vote, markets around the world responded swiftly and violently to the political and economic uncertainty that the “Leave” result presented. The British Pound lost roughly 10% against other major currencies, and several global stock markets were hit hard by the news.

While U.S. markets were quick to bounce back after the initial shock of the unexpected result, other global markets were not as resilient. The differing reactions fed a continuation of what is now a significant multiyear trend, that of U.S. stock market dominance over international markets. Despite continued volatility, the S&P 500 has managed to post a 2.7% gain through the first two quarters of the year. But the MSCI EAFE Index (which tracks non-U.S. markets, with a heavy emphasis on Japan and western Europe) has struggled, posting a 6.3% year-to-date decline, per Yahoo! Finance data.

If the trend of U.S. market outperformance continues throughout the remainder of 2016, then this will mark the fourth consecutive year (and sixth in the last seven) that U.S. markets will have experienced better returns than their international counterparts. And the underperformance has not been small, either; per Yahoo, a dollar invested in the international index at the end of 2009 would have returned just 1.8% through the end of Q2, whereas the same dollar invested in the S&P 500 would have returned a whopping 88.2%. Unsurprisingly, many investors have grown impatient with international investments and begun to question the wisdom of holding them in their portfolio in the first place.

The frustration is understandable, but a longer-term perspective paints a much different picture of the role of global exposure. While U.S. stocks have certainly been the stars of the investing world in the post-financial crisis period, they were the laggards in the years immediately prior—from 2002 through 2007, international stocks outperformed every year, with an average annual outperformance of 7.7%. Taking an even longer view, the analysis continues to look good for international stocks—in the 46 years that the MSCI EAFE has been calculated, the index has outperformed the S&P 500 in 24.

Source: Yahoo! Finance

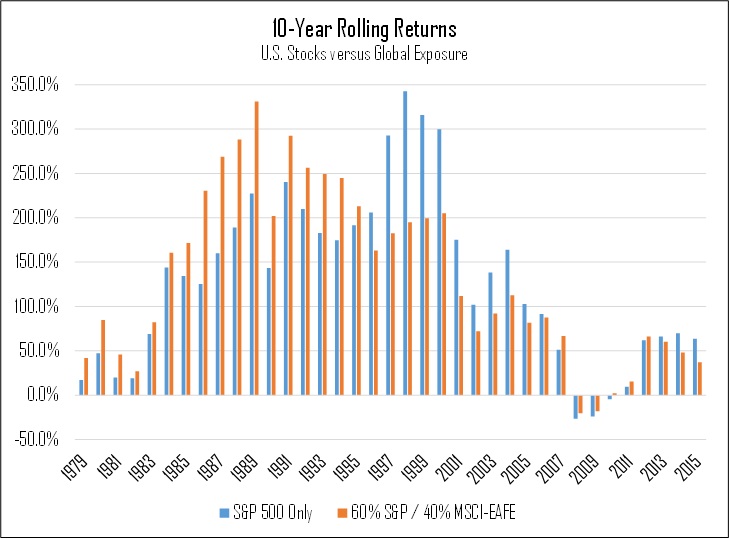

To better evaluate the long-term value of holding international stocks in a portfolio, we compared a U.S.-only stock portfolio to one composed of 60% U.S. stocks and 40% international stocks. Looking at historical rolling 10-year returns, we found that the portfolio with global exposure outperformed the U.S.-only portfolio in 23 out of 37 10-year periods, a strong beat rate of 62%.

Given the clear tendency for U.S. and international stocks to trade roles as the leaders of the global market environment, we think that now would be an inappropriate time to spurn international stocks. On the contrary, we think they could be primed for another period of outperformance over U.S. stocks, and that keeping a global perspective will continue to pay off over the long run, as it has in the past. Recency bias may be a strong psychological factor, but we shouldn’t let it guide our investing approach.

The views expressed are not intended as a forecast, a guarantee of future results, an investment recommendation, or an offer to buy or sell any securities. The information provided is general and should not be construed as investment advice or to provide any investment, tax, financial or legal advice or service to any person.