The financial planning process is, by its very nature, an exercise in exploring sensitive and delicate issues. But perhaps no topic generates as much discomfort and anxiety among clients as life insurance. In general, most people—especially younger, healthier individuals with young children—find it difficult to confront the idea of their own mortality, and they subconsciously underestimate their own risk as a result.

Of course, the unfortunate fact is that no matter how healthy or cautious we may be—and regardless of our family health histories—there is a certain level of risk that is simply impossible to avoid. Sudden illnesses, car collisions, and freak accidents do sometimes happen, and any responsible financial plan must take those risks into account.

The good news is that despite their natural discomfort, most Americans seem to understand the importance of life insurance in managing financial risks. According to a 2016 study from the research association LIMRA, 70% of American households carry at least some life insurance, a figure that climbs to 80% for households with minor children. Rates of life insurance coverage are on the rise, and they now stand at an all-time high, perhaps thanks to an increasing number of employers who provide group-based insurance plans to their workers. Unfortunately, however, even as the number of insured Americans has risen, the quality of that coverage has declined—LIMRA found that the average insured household carried enough insurance to replace just 3 years of income, down from 3.5 years in 2010.

But is that 3 years of income replacement enough, too much, or just right? Just how much life insurance should we aim to have? And when should we think about getting more, or perhaps less? While navigating the life insurance landscape remains at least as much an art as a science, it’s important to at least know the right questions to be asking.

Multiple approaches to insurance sufficiency

The first step in determining how much insurance is sufficient is taking inventory of your family’s expected future financial needs (in other words, projected future expenses). Because these needs can vary so widely from one family to another, a number of shortcuts have become commonplace in order to generate basic “life insurance need” estimates without having to engage in a full-blown financial planning process.

Most commonly, advisors or insurance salesmen will simply apply a standard multiple to the insured person’s annual income: a factor of between 6 and 10 times annual income is typical. This rule of thumb is essentially a simplified version of what is known as the “human life value” approach to life insurance sufficiency. The human life value method, as its name suggests, tries to determine how much an individual’s life is “worth”, in terms of some discounted amount of future earnings potential.

While the “human life value” approach is intuitive and easy to apply, it also comes with a number of shortcomings, and it often overestimates an individual’s actual insurance need. For people whose income far outstrips their annual expenses, a 100% income-replacement ratio might not be necessary. Covering basic living expenses might be possible with just half of the insured person’s annual income, or even less.

Most importantly, though, the human life value approach fails to consider other factors that will impact a family’s ability to cover its financial needs in the event of an untimely death. First, it generally does not consider any other assets—investments, houses—that might be available to help cover expenses. In other words, a family that has already saved a significant amount of money might not be as dependent on ongoing income as the human life value approach assumes. The method also often fails to consider the ability of a surviving spouse to earn income of his or her own. Some spouses are more vulnerable than others, whether because of health or low job skills, while others may be able to benefit from Social Security survivor benefits (especially those with minor children). Finally, the human life value approach fails to account for flexibility on the expense side of the ledger. Some families have very rigid expenses (e.g. high levels of debt repayment), while others might have large discretionary expenses that could fairly easily be curtailed if necessary. A full financial needs analysis will consider all of these factors and then some, and we therefore recommend that any insurance sufficiency analysis be performed as part of a broader financial planning process.

Other factors

Ultimately, the decision on an appropriate level of insurance coverage will require some fairly in-depth conversations and questions. If something did happen to a primary wage-earner, what would the surviving spouse do? Would they continue to work (or go back to work), or perhaps consider moving to a new house, new city, new state? Would they still want (or expect) to make the same levels of contributions to their children’s college tuition? Would additional child care expenses be necessary?

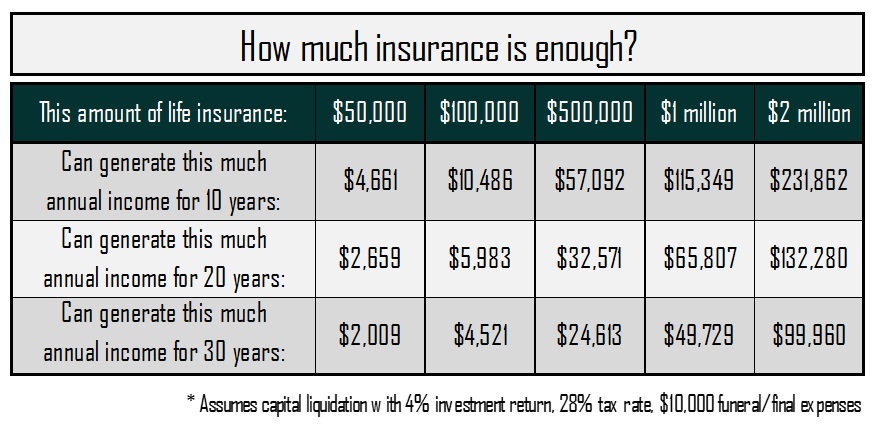

Also, how many years of expenses need to be covered? Are we simply trying to generate enough money to smooth things out for a few years until other arrangements can be made? Or will we be counting on insurance to cover multiple decades worth of expenses? Of course, the longer the horizon in question, the more the investment strategy with the insurance proceeds will begin to matter—how much risk the surviving spouse is comfortable taking (and what the prevailing market interest rates might be) can start to impact the necessary amount of life insurance coverage.

As should be clear by now, the process of determining an appropriate level of insurance coverage is less a mathematical equation and much more a qualitative discussion about lifestyles and desires. Like so many things in the financial planning world, acquiring life insurance is a process of finding the right balance between the art and the science.

Life insurance is complicated, and deciding how much coverage to obtain is only one part of the decision. Choosing between term life and whole life, how long a term policy to select, what types of riders to add to a standard policy, or even certain tax considerations (remember, insurance death benefits are paid out tax-free) are all important decisions that require thoughtful planning. At Cypress, we take pride in helping our clients think through their life insurance decisions, and how their insurance fits into a broader financial plan. If you have no insurance, or you don’t know if your current policy is a good one, we’re happy to help out.