In our most recent article, we presented an initial overview of budgeting basics, while promising to take a deeper dive into the practical side of building (and managing) a household budget. We’ll do just that in this quarter’s post, beginning by revisiting some of our initial recommendations from our last edition, and using those as a framework for building out your own from-scratch budget using a basic spreadsheet. We’ll also take a look at a high-level overview of a couple of the most popular online budgeting tools, to explain some of their benefits and drawbacks.

Knowing what to look for

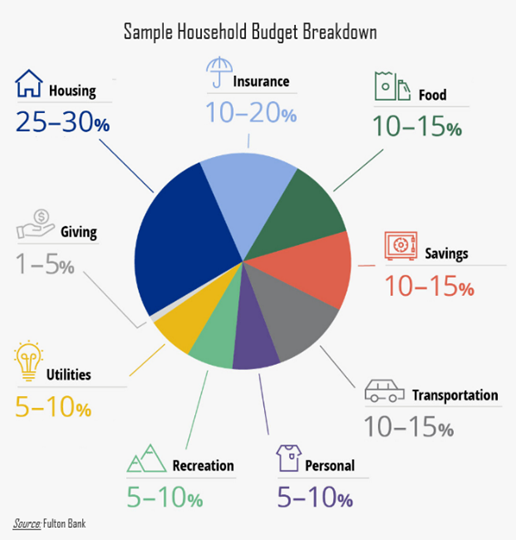

In our last piece, we recommended “starting at the finish line”, and working backward—this means setting a savings target first, and then fitting the other pieces around that target to make the math work. As a long-term strategy, this is still our recommendation. But it’s not a practical first step if you’re just trying to get a grasp on what your “today” budget looks like. In order to do that, we recommend using our “buckets” strategy, which we also introduced in our last newsletter. At Cypress, we typically focus on four major categories of expenses, each with their own specific line items that fill up those buckets: Home, Living, Discretionary, and Debt.

First and most important are the Home Expenses; these are generally repeatable, unavoidable expenses that are directly tied to an individual or family’s primary living space. They include large line items like mortgage (or rent), property tax, home insurance, and utilities (electric, cable, internet, water, etc), as well as maintenance items like condo fees, home repairs, landscaping, cleaning, and alarm systems. These home expenses are mostly recurring and therefore relatively easy to track. Most families have a pretty good feel for what these expenses are from month to month, so this is typically the easiest category to complete. The only exception here might be repair costs, which can be irregular (and often large) when they do arise.

Next is Living Expenses. These can vary somewhat widely from one household to another, but practically speaking, these include any group of expenses that are “required” for daily life (and therefore hard or impossible to cut out in a time of financial stress), but that are not directly tied to keeping the lights on in your house. The most obvious line items here include food and other groceries, health insurance, life and disability insurance (if applicable), cell phone bills, pet-related expenses, gym memberships, and car or other transportation costs (car lease or payment, auto insurance, car repairs, and fuel costs, plus possibly tolls and/or fares for rapid transit). Out-of-pocket medical expenses can also be a major line item here, especially for households with high-deductible health insurance, or those with high prescription drug costs.

As you might imagine, this category is where things start to become a little more irregular, and a bit harder to track. In order to properly add these expenses to a basic spreadsheet, it may be necessary to pull together several months’ worth of credit card bills, in order to see when and where your dollars are being spent.

On that point, the next category is your Discretionary Expenses, which is where many budgets start to go off the rails. The word “Discretionary” may not be a perfect descriptor, since some expenses here might be considered “absolutely necessary” in a discussion of where and how to start trimming a budget. Nevertheless, this category includes all expenses that could theoretically be eliminated in a time of great financial stress, even if only for a month or two.

Because spending patterns vary across households, there are dozens of different line items that could fall into this category, some of which are highly irregular, and might only be spent once a year (or less). At Cypress, some of the discretionary items we ask about are clothing, dining out (restaurants/take-out), gifts (including birthdays, weddings, and holidays), hair & beauty, entertainment, vacation/travel expenses, charitable donations, club memberships, books & music, and streaming TV services or other online subscriptions (news, music, etc). A few more are child care, parties, or miscellaneous “luxury” items like jewelry. For the novice budgeter, this is where things start to get daunting, and it may require consulting a year or more of bank or card statements in order to really get a feel for where your money has been going.

Sometimes, it can be helpful to “start anew”, and essentially ignore where your money has been going, and instead aim for where you’d like it to be going. Since the Discretionary category is the one that’s theoretically easiest to cut in a time of great financial need, it should also be the most fungible category during a budgeting process, and the one that affords the most “wiggle room”. If you’re unable to meet savings targets (or, worse, spending more than you earn), this is the first place to turn your attention.

Considering the leading online tools

The concept of “starting anew” leads neatly into a discussion of two of the most popular web-based budgeting apps, Monarch and YNAB (“You Need A Budget”). Both are subscription-based platforms with similar costs (~$100 per year), and both generally use some version of a “zero-based budgeting” approach to money management. But there are key differences.

For those who have used Intuit’s now-defunct Mint platform, Monarch is the most direct replacement. Like Mint, Monarch uses a holistic financial planning approach, aggregating all accounts to easily view household net worth, with a focus on monthly cash flow. Its tool can be a bit backward-looking by nature (largely serving as a “transaction tracker” that allocates expenses to specific budget buckets as they arise), which can limit its usefulness for someone who is trying to build a forward-looking budget, starting from scratch. But, its flexibility to set a number of different financial goals has been a hit with many users.

YNAB, on the other hand, is a heavily structured rules-based tool with a singular focus on budgeting. The tool is forward-looking, with a key goal to “give every dollar a job”. As a result, YNAB is much more granular, and many new users report some level of frustration with the platform’s steep learning curve. And, unlike Monarch, there is minimal support for any tracking of investments or other planning functions. YNAB is for budgeting and budgeting alone, and it is rigorous in its pursuit of its goals, especially debt reduction. It is also prescriptive in a way that helps identify irregular expenses, which can often be hard to plan for in the budgeting process.

Ultimately, there is no one-size-fits-all budgeting answer, but the vital first step is to make an honest accounting of all relevant expenses, both the regular (recurring) ones and the less frequent (but often large) bills. If you need our help finding a budgeting tool that works for you, please feel free to reach out.