NOTE: The following piece is intended for current and former employees of Lockheed Martin Corporation. Our founder, Jeff Jones, is a former Lockheed Martin engineer, and we at Cypress are privileged to work with a number of Lockheed employees and alumni. If you are interested in learning more about our services, please Contact Us or Schedule a Meeting.

The 401(k) plan offered by most employers today has become the foundation of retirement savings for the majority of Americans. However, the 401(k) itself is a relatively young savings tool that has become what it is today almost by accident. Just over 30 years ago (in 1978), Congress passed a simple Revenue Act that included a provision—Section 401(k)—that gave employees a tax-free way to defer compensation from bonuses or stock options. That provision was subsequently expanded in 1981 to allow employees to contribute to their 401(k) plans directly through regular salary deductions.

This expansion fueled widespread adoption of the 401(k) plan in the early 1980s, as employers gradually realized that the plans were cheaper and more predictable to fund than traditional pension plans. While the shift was touted as giving employees greater control of their own financial futures, in reality it shifted the responsibility for funding retirement from the employers onto the employees. Fast-forward 30 years, and this trend has accelerated to the point that the 401(k) has all but replaced traditional pensions as the primary vehicle for retirement planning.

When utilized effectively and early enough, the 401(k) can be a powerful solution to charting your own course to retirement. But understanding the ins and outs of the plans can be vital, in order to maximize the potential benefits. The details matter, so it's important to dive deep into those details. With that said, let’s take a look at the 401(k) plan offered to you through Lockheed Martin:

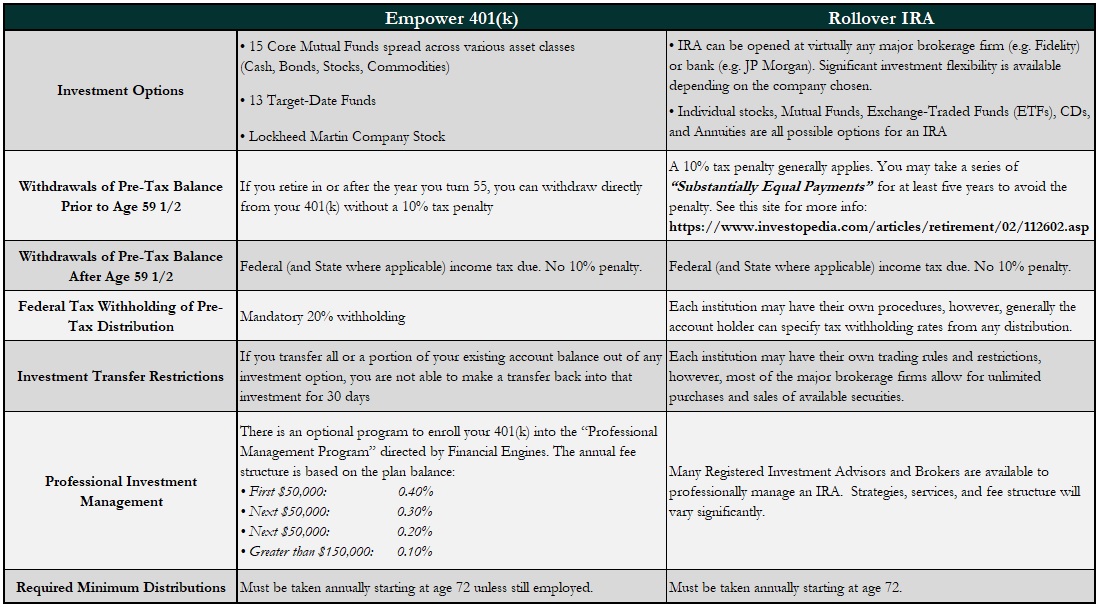

Empower 401(k)

Over the years, a slow-and-steady approach of living below your means, socking away a portion of your earnings into the PSP, SSP, and/or CAP (and collecting the full Employer Match along the way!) has hopefully left you with a healthy balance in your account. After you walk out the door for the final time, one of your biggest retirement account decisions will be whether you’d like to keep your balance inside your 401(k), or roll the funds to an Individual Retirement Account (IRA). Here are the most important points to consider regarding this important decision.

Features of the Empower 401(k) Post-Retirement

• Investment Options include 15 Core Mutual Funds spread across various asset classes (Cash, Bonds, Stocks, Commodities) and 13 Target Date Funds

1. If you have an outstanding loan, the balance will become due and payable in full on the date you retire from the Company. In order to avoid defaulting on your loan and paying taxes on it as a distribution from the Plan, and also to be able to roll over the full amount of your account balance, you must pay off your loan in full.Here are some other important points to consider upon retiring with a 401(k):

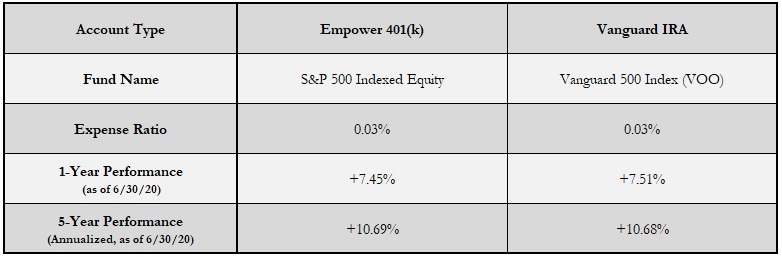

2. Many of the investment options within the Core Empower Fund Lineup can be re-created within an IRA. The S&P 500 Indexed Equity is an example of a mutual fund that has many similar options outside of the 401(k).

Source: Morningstar

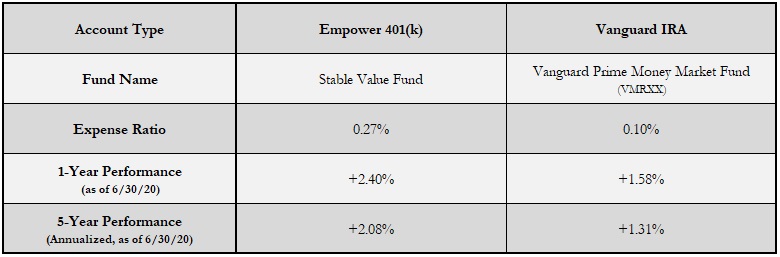

For more conservative investors, however, it is more difficult to find a guaranteed savings vehicle in an IRA with the same level of yield and liquidity that is provided by the Stable Value Fund.

Source: Morningstar

3. If you have balances in either the “Roth 401(k)” or the “After-Tax 401(k)”, rolling these out of Empower will require opening an entirely separate account at the IRA custodian called a Roth IRA. Doing so will preserve the favorable “Post-Tax” status, and also allow for any future earnings on the balance to also be tax free. Any balance kept in an “After-Tax 401(k)” at Empower is actually very tax-unfavorable, as growth in those investments will still be subject to future taxation. This can be avoided by processing an “In-plan Roth Conversion” at Empower, or by rolling to a Roth IRA.

As you can see, the 401(k) plan has many attractive features while you’re employed at Lockheed Martin and eligible to contribute. As you approach retirement, knowing your options when it comes to investments and the different potential tax treatment of distributions is critical to a sound retirement strategy. A qualified financial planner can help you sort out these things in the context of your overall financial plan and income needs. If you’d like to discuss your options regarding your Empower 401(k), Please Click Here to schedule a complimentary introductory call with a fiduciary financial planner from Cypress Financial Planning.