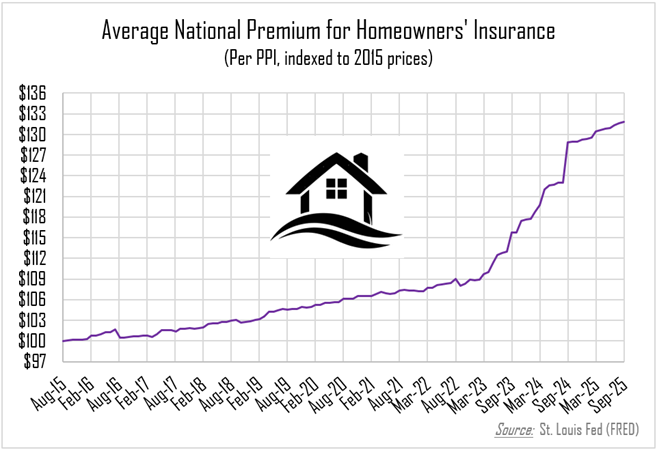

For most families and households, the primary residence represents one of the largest assets on their balance sheet, and it is certainly the largest single purchase (or investment) in most individuals’ lifetimes. Protecting that asset, then, should be a consistent and thoughtful consideration for the homeowner. And yet, more often than not, property insurance is something that is obtained once (at the time of the initial purchase), and then infrequently reconsidered, if ever. But the property insurance industry is constantly evolving, and coverage rates and terms are changing along with it, especially as some of the larger insurers have had to adjust to more frequent large losses (due to serious storms, wildfires, or other natural disasters).

Understanding what your insurance does and doesn’t cover, how to evaluate if you have gaps in coverage, and making sure that you’re getting an appropriate value for your insurance dollar are all key considerations. This primer will aim to summarize the main concerns, in order to help you make informed decisions.

What is actually covered?

Homeowners’ insurance policies can vary widely, but generally speaking, there are five major areas of coverage to be considered: dwelling, other structures, personal property, liability, and loss of use. The dwelling coverage is, of course, the most intuitive, and it is the area of coverage that most purchasers focus on most closely. This primary coverage will protect against damage to the structure of the home, with replacement cost the typical guiding principle (more on that point later). The second area of coverage, “other structures”, is typically tied directly to the value of the primary structure. Most policies will set this coverage at a set percentage of the primary dwelling (10% of the primary dwelling coverage is a common starting point), and this adds on top of the dwelling coverage to cover damage to any outbuildings like detached garages, sheds, fences, or other permanent outdoor structures. Personal property is another secondary coverage amount, similar in principle to renters’ insurance, covering the value of the belongings inside the house (as opposed to the physical structure itself).

Most policies will also include additional coverages that do not specifically compensate the owner for damage to the property, but can help protect against other common housing-related issues. The first is liability coverage, which can help to protect the homeowner if someone is injured or otherwise harmed while on the homeowners’ property. This is important in all cases, but it can be particularly important if the homeowner has other assets outside of the residence that may face claims if injury-related costs are high enough. Finally, “loss of use” coverage can help to pay for temporary living expenses if your home becomes uninhabitable due to damages or other factors. The primary insurance coverages will help to pay for the repair costs, but they will not cover the temporary living expenses while the work is ongoing. For lengthier repairs, these costs can be a significant hardship.

Different insurers may have different standard coverage levels for many of the secondary (non-dwelling) coverages, so making sure that different policies are being compared on an apples-to-apples basis is always important.

How is insurance priced, and where can gaps occur?

As mentioned above, the guiding principle behind dwelling-based coverages is the replacement cost of the structure or item in question. This distinction has become key in recent years, as the impact of inflation over the last several years has led construction costs (and materials costs) to soar. Coverage that may have been adequate five years ago might not necessarily automatically adjust to cover current economic realities, so periodic reconsideration of coverage limits is vital.

Beyond the expected costs of replacement, different insurers may price the risks of loss differently. A few different areas of consideration will be the age and condition of major systems (roof, plumbing, electrical), local risks (like weather and/or crime), and claims history on the property (or similar nearby properties). Insurance premiums will also vary based on the amount of the deductible, which different insurers will set at different levels. Not all insurers will consider these risks the same way, so it can be important to shop around and see.

Of course, even with a properly crafted and selected insurance policy, coverage gaps can occur over time. For “other structures” coverage, significant additions or renovations to exterior improvements may overwhelm the standard coverage limits, and the insurance company will not know to adjust your coverage (and premium) unless you alert them first. Similar gaps can develop with “personal property” coverage, especially if new acquisitions are made. Many insurers will require that individual items above a certain threshold value (say, $3,000) be separately scheduled and appraised, and specifically listed on the policy in order to be covered. Otherwise, standard policy limits will apply, and things like artwork, jewelry, and antique furniture may not be fully protected.

Finally, liability coverage may become inadequate if and as the homeowners’ total net worth grows over time. Eventually, a separate “umbrella” insurance policy may be required, in order to make sure that all assets are protected.

Other considerations

Depending on the local market, some “perils” (like flood or earthquake) may be relevant but are typically excluded from standard policies and require separate coverage. Local ordinances may also change over time, meaning that even smaller damages can come with substantial costs if remedial work is required in order to meet current code.

Homeowners insurance is, ultimately, a core part of a household’s financial foundation. Regular reviews, thoughtful comparisons, and a clear understanding of potential gaps can help ensure that when the unexpected happens, your insurance performs the way you expect it to. Of course, the analysis must also include a consideration of the insurer, in addition to the policy itself. Financial stability, customer service and claims responsiveness, the consistency of underwriting (avoiding the risk of a sudden policy non-renewal), and experience with specific local dynamics are all worth considering when selecting an insurer and a policy. A difficult claims process can cause needless headaches and wasted time, and paying a few more dollars in an annual premium can sometimes be well worth the added peace of mind.