As the third quarter reached its end, the most recent short-term federal spending agreement (originally reached in March) expired, sending the government into shutdown mode once again. This closure marks the 11th such funding gap since 1980—when a legal opinion first began to require it—and the third since 2018. The vast majority of these shutdowns have been brief, with 7 of the prior 10 resolving in 5 days or fewer. This latest instance seems poised to become the 4th lengthy shutdown in history, joining the closures of 1995-96 (21 days), 2013 (16 days), and 2018-19 (35 days).

But what, exactly, is a “government shutdown”, and what does it typically mean for the economy and the stock market? We’ll take some time to look at a few of the more recent shutdowns, in order to help explain what to expect over the coming days or weeks.

Understanding shutdown basics

Most agencies of the U.S. government operate under a series of annual or multi-year appropriations passed by Congress. Occasionally, when these appropriations stall for one reason or another, a “continuing resolution” or other short-term patch can be reached to allow for critical agencies to be funded while a more permanent agreement can be negotiated. If such a resolution expires and is not replaced by a similar agreement or other appropriations bill, then all “non-essential” parts of the government must halt operations until such funding is restored.

The line between “essential” and “non-essential” can shift over time, but as a general rule, “emergency personnel” continue to be employed—these include active duty military, law enforcement, health care professionals working in federal hospitals, and, perhaps most notably to average civilians, air traffic controllers that keep our aviation system functioning. Some agencies will operate with “skeleton” crews, including the National Weather Service, Army Corps of Engineers, and parts of NASA. The United States Postal Service is a self-funded agency that usually remains open, and, somewhat controversially, members of Congress continue to be paid.

Essentially all other federal agencies are required to temporarily cease operations, furloughing rank-and-file employees (putting them on temporary unpaid leave) and scaling operations back to their bare essentials. While the shutdown continues, facilities like national parks and federal monuments typically remain closed, and most economic data releases and other agency communications will be paused. While furloughed employees generally receive back pay once the government reopens, there is not necessarily any explicit guarantee, and such back pay is officially reliant upon any eventual spending agreement that Congress may reach.

This uncertainty can, at times, lead to higher rates of absenteeism among federal employees deemed “essential”, as the unfortunate reality of working for indefinitely-delayed pay begins to set in. In the 2018-19 shutdown, for example, the TSA reported that roughly 10% of its officers called in sick at one point or another, leading to significant flight delays at several major airports.

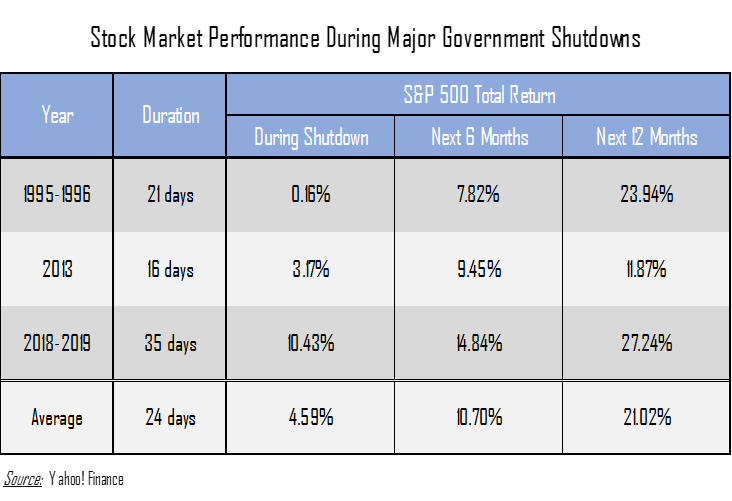

What’s the typical impact on markets and the economy?

Federal spending represents an increasingly large portion of American economic output (at roughly 23% of GDP in 2024), so any disruption to that spending will be noticeable. Because some of the lost output is eventually recouped once the government reopens, though, the actual impact on economic growth tends to be relatively manageable—around 0.1% or 0.2% per week of the closure, according to recent Morningstar estimates. That said, such estimates are rough at best, in part because some data cannot be properly collected while government offices are closed.

Regardless, perhaps due to a recognition of the limited economic impact, the stock market also tends to take news of government shutdowns in stride. In fact, in our most recent extended government shutdown (the 35-day closure in 2018-19), the S&P actually gained more than 10% during the month-long closure, then continued to post an additional 27% return over the ensuing 12 months once the government reopened. That advance was ultimately interrupted by the COVID-19 pandemic, but by that time, the shutdown was a distant memory. If we widen the view to consider the three lengthy government shutdowns mentioned earlier, the pattern seems to hold, with the market rallying in the aftermath of all three closures, usually substantially. The average six-month return after reopening has exceeded 10%, with the average 12-month return clocking in at more than 20%. Naturally, this is a limited data set, and not nearly enough to predict that shutdowns are “good for the market”, but they are at least sufficient to put our minds at ease and hopefully convince us that shutdowns are not to be especially feared.

What to expect next

Of course, every shutdown is different, because every economic (and political) environment is different. Against the 2025 backdrop of DOGE and a White House administration seemingly determined to decrease the overall size of government, it’s possible that the economic disruption from our current shutdown could be more permanent than in previous closures, perhaps by design.

One could argue, though, that the Federal Reserve has already anticipated this potential outcome, preemptively loosening monetary policy with their September rate cut, in order to hopefully give the economy some breathing room in case a more damaging shutdown does arise. Loose monetary policy does not replace government spending one-for-one, but it can encourage growth from other (non-government) sources, helping to offset a decline in one area with an increase in another.

In the meantime, there’s little to do but watch and wait, as the political sideshow that has defined this year so far takes another turn. This shutdown was predictable, after all, especially after the divisive process that led to the passage of the massive “One Big Beautiful Bill” in July. The terms of any settlement to this current stalemate may ultimately prove to be more important than the duration or nature of the shutdown itself. Democrats have seemed to draw a line in the sand over an expansion and/or restoration of health care spending, particularly an extension of Obamacare subsidies that would otherwise expire at the end of the year. From a financial planning perspective, that alone could be a major area to watch.