In the 2024 election campaign, President Trump ran on a wide-ranging platform that included promises of both increased tariffs and sweeping immigration reform. In the initial weeks of his term, action on both fronts was somewhat limited, and there was an expectation among most economists and analysts that his ultimate trade policies would rely on more “targeted” tariffs, and not the “blanket” rates he had espoused on the campaign trail. But in the past month, those expectations have been laid to waste, as the administration announced a series of aggressive tariff hikes, increasing each week in both range and severity.

Most recently, on what the Trump team labeled “Liberation Day” (April 2nd), the U.S. imposed both a baseline 10% tariff (applying to all trading partners, taking effect on April 7th) and a complicated system of reciprocal tariffs aimed at more than 50 individual nations, based on certain specifics of that country’s trade relationships with us (taking effect on April 9th). Those reciprocal tariff rates ranged from 11% to as high as 50%, including high rates on many Asian nations, from which the U.S. has long imported a wide variety of apparel and other miscellaneous consumer goods. With China specifically, their new 34% reciprocal tariff appears to be in addition to their existing 20% baseline tariff, bringing their overall effective tariff rate to nearly 60%. The stock market reaction to these tariffs was swift and severe. The S&P 500 fell by nearly 5% on the day following the tariff announcement, leading many analysts to mockingly refer to “Liberation Day” as “Obliteration Day”. A similar decline followed on the ensuing day, with the cumulative losses erasing nearly all of 2024’s gains and instantly sending the index down into bear market territory.

The justifications for the tariffs

In sum, the new Trump tariffs are expected to bring average U.S. tariff rates to their highest levels in more than 100 years, since William Howard Taft was in office. White House communication has mostly relied on three justifications for the tariffs: they will enhance national security, they will bring manufacturing jobs back to the U.S., and they will restore balance to a trade environment that the Trump administration views as fundamentally unfair. A fourth reason that also cannot be ignored: the Trump administration hopes to raise enough new revenue via tariffs to pay for an extension—and likely expansion—of their 2017 tax cut package, many provisions of which are scheduled to expire at the end of this year.

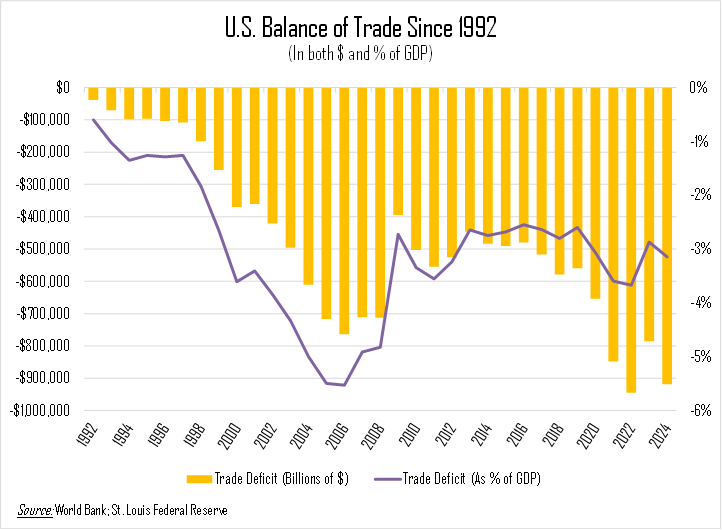

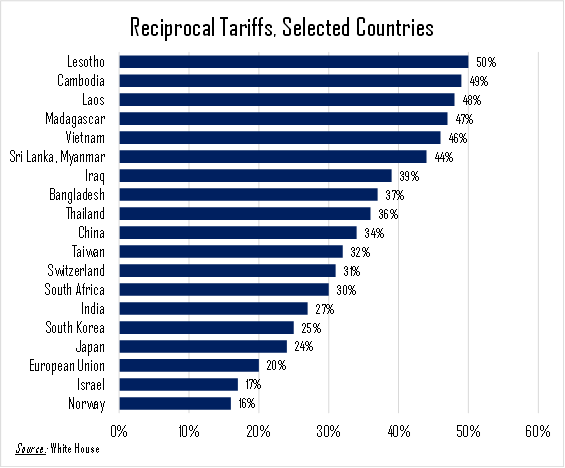

To unpack all of these justifications would take more space than we have available in this format. However, we can attempt to address a few high points. First, on fairness, there is clearly some room for improvement. The U.S. trade deficit has consistently expanded over the last three decades, and currently stands at a level of about $1 trillion per year (meaning that we import substantially more goods from other nations than they purchase from us). As a percentage of our total economy, that figure has actually tightened somewhat in recent years—at its “worst” level, in 2005, the deficit represented more than 5.5% of U.S. GDP, but that level has stabilized at an average of 3% per year over the last 10. Still, that’s a wide gap, and by some estimates, more than 85% of our trading partners have “advantageous” trade deals with the U.S. Some amount of leveling is easy to justify, but any attempt to eliminate the trade deficit entirely is undesirable and likely impossible. The U.S. runs consistent trade deficits in large part because we are the world’s largest consumer economy, and our residents buy incredible amounts of products of all types, many of which do not (or cannot) exist inside our borders. Take, for example, the tiny nation of Lesotho, which is subject to one of the highest reciprocal tariff rates under the Trump plan, at 50%. With a per-capita GDP of just $1,000, Lesotho’s consumers cannot afford much in the way of imports from the U.S., and they therefore purchase practically nothing. But their economy relies heavily on the production and trade of diamonds and denim (roughly 10% of its national economy), and the U.S. imports nearly $240 million of goods from the nation each year. Essentially all of this amount represents a trade deficit, and under the new tariff calculations, this deficit qualifies Lesotho as an abusive trade partner, subject to a 50% “reciprocal” tariff.

Not all countries are like Lesotho, of course, but its case study can help to illustrate the difficulty of attempting to eliminate all trade deficits. The U.S. demand for certain products far outstrips our ability to create them, and we can’t simply build diamond factories overnight in order to compete with Lesotho’s natural resources (lab-grown diamonds may be a growth industry in recent years, but they still command a much lower price tag than their naturally occurring counterparts). Some products and services simply cannot exist in every country, and this is in fact one of the benefits of trade; it will not always be “fair”.

The outlook for jobs

While an imperfect example, there is a lesson in Lesotho for the “job creation” argument, which is one of the administration’s primary justifications for tariffs in the first place. There are, of course, many industries

and products that have competitive multinational markets, and bringing production for some of these goods back to the U.S. could absolutely restore at least some amount our nation’s manufacturing capacity. President Trump’s electoral base consists of many of the areas that have been hardest hit by the decimation of our manufacturing industries, as outsourcing of production over the last 30 years has left many rust-belt towns and cities in relative ruin.

But bringing those jobs back is not an overnight decision, nor does the capacity to create those jobs automatically show up. The process of globalization took decades to complete, and it cannot be instantly reversed. Companies will only make the required investment in factories and building new supply chains (investments that in some case can be massive) if they believe that the proposed tariffs are credible and reasonably permanent. It will take years for the companies to receive payback on any investments made, so they need to be sure that the tariffs will be in place long enough to make back their money.

So far, the commentary from most corporate CEOs has been mixed, but the general impression is that they do not consider these tariffs to be permanent. This means that any jobs that might arrive as the result of the tariff increase are a long way off, if they arrive at all. Furthermore, the broader labor market backdrop needs to be considered. Unemployment figures are currently at one of the strongest points in history, with rates at or near historic lows. We recently exited a COVID-fueled period of incredibly tight labor market conditions, whereby the number of job openings outpaced the number of unemployed workers by a ratio of more than 2 to 1. While this balance has gradually come back in line with historic norms, the labor market remains extremely tight, and few Americans are actively looking for new work. As it is, we are relying heavily on immigrant labor to meet our needs. All else equal, if these tariffs are indeed made permanent, the new tax on imports will almost certainly be inflationary, especially while we wait for new capacity (and new jobs) to come online.

That would be a bit ironic, given that exit polling after the 2024 election indicated that voter frustration with inflation was a heavy factor in Trump’s return to power. And while inflation is not assured, since projecting any economic impact depends entirely on how people both inside and outside the U.S. respond to the tariffs, in a tight economy that’s already at (or near) “full employment”, the jobs argument falls at least somewhat flat. That leaves us with the “fairness” argument, which is likely where this all ultimately lands. If the Trump administration is able to use its threat of reciprocal tariffs to get other countries to renegotiate existing trade deals in order to benefit the U.S. consumer, then the ultimate impact of this entire episode could absolutely be to lower inflation, increase U.S. production capacity, and strengthen the overall economic outlook. But the longer these tariffs are in place, the more complicated the picture becomes. The administration is walking a tightrope to be sure, and the implications are massive.

Addressing the market impact

Regardless of the economic impact, the market reaction so far has been swift and negative. U.S. stocks had already experienced their weakest quarter in more than three years in Q1, and “Liberation Day” sparked back-to-back daily losses of roughly 5% for the major indexes. This dramatic reversal of fortune for a market that performed so well in 2023 and 2024 has been shocking for market participants, many of whom are now wondering what comes next.

While large one-day moves like these are uncommon, they are not unprecedented. On three separate occasions in the last 20 years, we have seen a cluster of these sorts of sudden drops: in 2008-09 during the financial crisis, in 2020 after the initial COVID lockdowns, and in August 2011, following a downgrade of the U.S. government’s credit rating amid a broad debate about the government’s debt ceiling.

It’s the 2011 scenario that we think is the most instructive for our current purposes, for a variety of reasons. The political environment at that time was similarly fraught, with “Tea Party” loyalists insisting on large and immediate spending cuts, and some even proposing a constitutional amendment to require balanced budgets. Despite the turmoil, the market had remained strong, entering August 2011 with a 20% gain over the prior 12 months (and 36% over the prior 24). When the debt rating downgrade occurred, the shock of the headline gave a market ripe for a pullback an excuse to correct, and to do so quickly. Twice in three days, the market fell by 5% or more, and headlines were broadly negative, focusing on the decline of credibility of the U.S. government and its commitment to its obligations. Alas, the market quickly shook off the shock and recovered, rising by nearly 15% over the next 3 months, 28% over the next year, and 58% over the next two years. These kinds of bouncebacks are of course never assured, but the U.S. stock market has a long history of performing best when people expect (or fear) the worst. And there are still plenty of reasons for optimism.