Heading into this past November’s presidential election, by most traditional metrics, the national economy was strong and thriving. GDP growth was positive, inflation was back down near the Fed’s long-term target, and strong consumer spending data had added fuel to a persistent stock market rally that continues to lead the major indices to all-time-high levels. But according to exit polls conducted by Edison Research, two-thirds of voters described the state of the economy as “poor” or “not so good”, and 31% of those polled cited the economy as their most important issue. Of those who prioritized the economy, a whopping 79% favored Donald Trump, giving a strong indication that the lingering impact (and memory) of the inflationary period from 2021-22 was a driving force behind voters’ desire for change at the ballot box.

That apparent economic puzzle—strong ongoing data, but stubbornly negative consumer sentiment—has been a challenge for politicians and economists alike to navigate. It remains top of mind for a Fed board that would like to continue normalizing interest rates, but that is wary of stoking a new wave of inflation, or at least worsening an already-dour national economic mood. We’ll take a minute to sort through the puzzle, unpacking what it is that has people still feeling so anxious.

What’s the deal with inflation?

Fundamentally, the puzzle can seemingly be solved with one observation—yes, the rate of inflation is down, but prices are not. Consumers are always anxious about rising prices, and inflationary periods can often have a very long shadow and a lasting impact on the national mood. It can take years—if not decades—for consumer behavior to recover, and for consumers to again feel comfortable about the stability of the economy.

To get a better feel for what the cumulative impact of recent inflation has been, we’ll take a dive into the Bureau of Labor Statistics’ (BLS’) CPI calculations to see exactly where prices have been, and where they are now. As an example, we’ll consider grocery prices (which the BLS refers to as the “Food at Home” component). With an 8% weighting in the CPI, groceries are one of the largest influences on measured inflation, and of course one of the most noticeable items for the everyday consumer, since all individuals purchase groceries, and tend to do so fairly often.

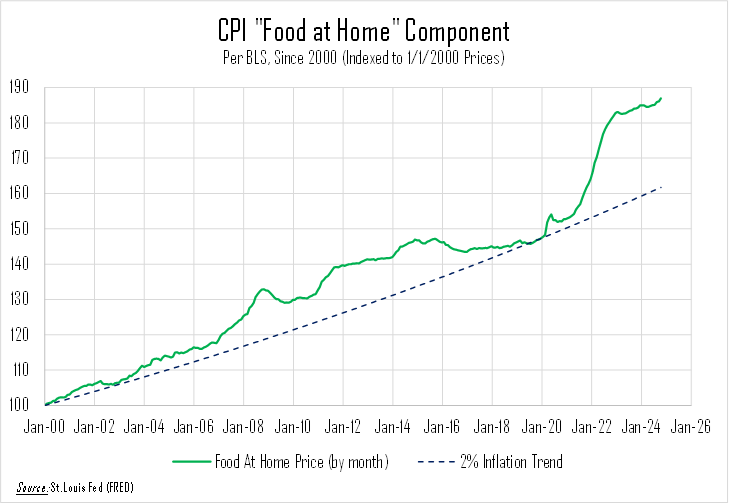

Before 2020, grocery prices had been remarkably stable, remaining essentially flat for 5 years, from 2015 to 2020 (prices increased by only 0.4% over that time period). The price stability may have presented a false sense of comfort in a very complex market, but it was stability nonetheless. Widening out further, dating back to the turn of the millennium in January 2000, the 20-year average grocery price inflation was 1.95%, per BLS data, essentially right in line with the Fed’s long-run 2% inflation target.

Of course, the next five years presented a decidedly different picture. As the repercussions of the COVID-era lockdowns worked their way through the economy, grocery prices surged in a way that we rarely see. For the 12-month period from August 2021 to August 2022, prices for “Food at Home” increased by 13.5%, the highest year-over-year figure since 1979 (and one of the highest figures in recorded history). Inflation eventually cooled to a more manageable level, but the damage was done.

Entering 2025, the cumulative grocery inflation over the past five years has been roughly 27%, where we “should” have expected just 10%, based on the pre-COVID trend. Given that prices are now more than 15% above where we might have expected them to be, even if we enter into a period similar to that from 2015-2020, with zero price inflation, we will still see grocery prices higher than the pre-COVID trend might have predicted, by about 5%. In order to come back down to the pre-2020 trend line, prices will have to remain flat until May 2032, or else prices will have to start trending back downward, which they rarely do on a sustained basis. Other goods and services have of course experienced similar price trends, so it’s not just the grocery store we need to be considering. But, since it’s such a visible cost for so many people, it’s an important dynamic to study.

What’s the impact on the consumer?

It’s easy to point at this inflation and say that “wages haven’t kept pace”, except that’s not entirely true. Per BLS data, national average wages for private workers have increased by 25.2% over the last five years, just barely behind the 27% cumulative inflation we saw for groceries. The problem is that wage growth alone does not determine out-of-pocket spending capacity, since taxes do take a bite. And, of course, not everyone is a wage earner. Retirees and other individuals on fixed incomes are a large portion of the consumer base (and the voting public), and they do not benefit from higher wages. Also, not all jobs saw the same “average” wage growth, so workers in industries with below-average pay increases have consistently fallen behind.

Of course, when consumers can’t keep up with the costs of the goods they purchase, compromises become necessary. Now that the COVID stimulus money has been fully exhausted, consumer debt delinquencies have begun to rise, and spending in non-essential areas has come under pressure. More and more individuals are having to strain and cut costs in order to “make ends meet”, and research shows that this sort of behavior can often become permanent.

According to data from the National Bureau of Economic Research (NBER), generations that lived through the inflationary period of the 1970s remain, even decades later, much more anxious about inflation (and therefore much more cautious about other spending/savings decisions) than the generations that followed them. Their faith in economic stability and prosperity was permanently altered by their lived experience, and it’s entirely possible that the recent inflationary period will leave similar “scars” for the younger generations over the coming decades.

Eventually, if price stability prevails for an extended period, memories will shorten and the national mood will improve. But ironically enough, some of President Trump’s campaign proposals (particularly on tariffs and immigration) would be quite inflationary, if taken to the extremes he discussed on the campaign trail. Most economists believe that the actual policies enacted will be more measured and targeted, but in the meantime, building in a little bit of extra budgetary flexibility (if possible) is probably a good idea.