For much of the last 3 years, economic conversations and headlines have been dominated by concerns about inflation and its impact on household budgets. Understandably, Americans have become increasingly concerned about their ability to make ends meet, and their growing anxiety is exacerbated by the fact that many individuals simply do not have a good grasp of their income and expense profile to begin with.

Budgeting has never been a favorite pastime for anyone, and while the statistics have gradually improved in recent years, the CFP Board still reports that 40% of recent survey respondents have never had a formal budget, even though they realize the importance of the exercise. This gap in understanding makes it difficult for people to determine how—and how much—to adjust their spending when price increases really start to bite. In our next two newsletters, we’ll discuss budgeting basics, including what does (and does not) work, while also providing tools that could help even the experienced household budgeter.

How to get started

There are so many potential moving parts in a household budget that it’s often hard to know where to start. As a result, most household budgeting happens on a day-to-day or week-to-week basis, with only minimal long-term planning or tracking. This approach can be both daunting and exhausting, and it creates a couple of obvious drawbacks. Most notably, a short-term budgeting focus does a poor job of accounting for unforeseen changes to income, or unexpected large expenses. It’s hard to establish an adequate emergency fund—not to mention save for retirement—if you don’t know what your target is, or what actions it takes to hit it.

Perhaps counterintuitively, then, we recommend starting at the finish line, and then working backward. Most budgeting processes—even some of the good ones—put “savings” as the last item. Once all of the major expense categories are covered, “savings” is whatever happens to be left over at the end of the exercise. From a long-term perspective, this is exactly backward, and almost guarantees that savings will always fall short of their target. It’s far better to “pay yourself first”, by determining a set savings amount (say, 15% of salary), setting that aside off the top, and then crafting a household budget within the remaining amount.

Then, perhaps even more importantly, it’s rarely a good idea to try to budget “to the penny”. Expenses can and do fluctuate from month to month, especially during times of economic uncertainty. If your electric bill happens to come in $25 or $50 higher than usual in a given month, you’ll want to have enough flexibility to compensate for that in another area. So, any budget should recognize this variation and adjust accordingly, perhaps setting for an “average” figure but with wiggle room for some amount above or below.

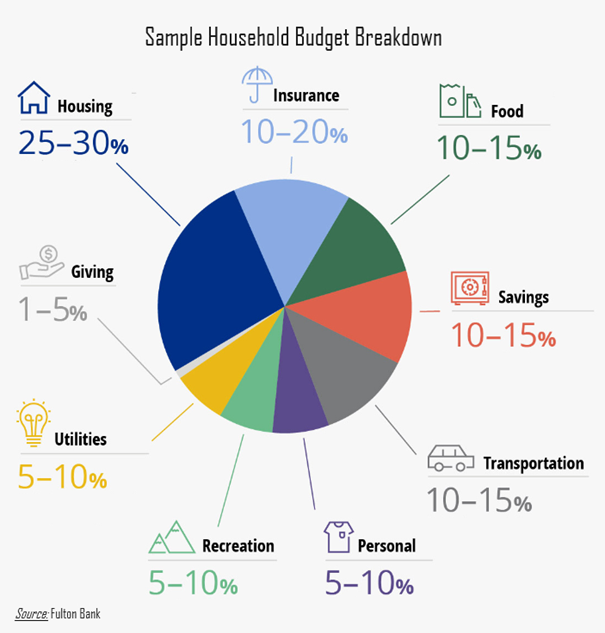

The initial budgeting process is easiest when we don’t try to account for every single individual expense, but focus instead on categories or “buckets”. At Cypress, for example, we start with three or four major categories: home expenses, living expenses, discretionary expenses, and debt repayments (if applicable). Home expenses are those tied directly to the primary living space (mortgage/rent, utilities, home insurance), living expenses include all other “required” expenses not explicitly tied to the home (food, clothing, transportation, medical expenses, personal care), and discretionary expenses include “everything else” (travel, entertainment, dining out, charitable donations, and more). For those who may be struggling with the scope of the budgeting process, setting target numbers for the overall categories—instead of the individual budget line items themselves—can be a very helpful exercise.

Furthermore, it’s incredibly important to remember to budget for irregular expenses. Most households (even those without a formal budget) are reasonably good at accounting for the expenses that come with regular monthly bills. But the “other” expenses are where things start to go off the rails, and therefore where savings goals start to fall apart. There are any number of these irregular expenses, some of which are larger than others. Some may recur annually or semiannually (things like vacations, home repairs, car maintenance, holiday gifts, insurance premiums, and health care expenses), whereas others might only come along once every several years, or once ever (school tuition, weddings, home renovations or additions, automobile purchases, etc). If these items aren’t built in to your budgeting process, then some level of financial strain is inevitable.

Budgeting guidelines and rules of thumb

When in doubt, some basic industry guidelines can provide a solid starting point for discussions. These rules of thumb can be limiting—not all areas of the country have similar costs of living, and every household is unique—but they are based around reasonable logic. One common budgeting approach is the “50-30-20” approach, which apportions 50% of income to “needs”, 30% to “wants”, and the remaining 20% to savings and/or debt repayment. It’s not a bad starting point, although it does leave some significant room for interpretation between what is a “want” versus a “need”. But by making at least some allowance for the fact that discretionary expenses are a real and necessary part of a household budget, this approach has understandably gained in popularity in recent years.

Another common budgeting guideline actually comes directly from the banking world, where most mortgage lenders request (or require) that no more than 28% of a household’s gross budget be directed toward housing costs (including principal, interest, taxes, and insurance). That 28% guideline has often been interpreted somewhat more broadly to suggest that roughly 30% of a household budget should be directed toward direct housing costs.

Other considerations

Unfortunately for novice budgeters, one of the most popular online budgeting tools (Intuit’s Mint) has now been discontinued. A variety of other tools are still available (including Cypress favorite eMoney, or paid options such as Quicken, YNAB, or Monarch), all of which come with certain pros and cons. In our next newsletter, we’ll take a deeper dive into some of those tools, while also discussing some “manual” options.